I’m not a magazine reader, so it came as news to me when someone on Twitter said that Dave from Strong Money Australia gave a shout out to a few Aussie FIRE bloggers (including me – thanks Dave!) in a Money Magazine story about the FIRE movement in Australia.

Of course, I was anxious to read it, so I downloaded the Libby app and borrowed Money magazine from the library. (That’s another $9 off my “Earn my rates back” reading quest. ) I’d recommend reading the article for yourself, but in a nutshell, they interviewed 7 people who have either finished the FIRE path or are on their way along it. All but one were younger than me and all had different ways of navigating the path towards total financial freedom.

It made me wonder what I would have said, had I been interviewed. I’ve been a single mother for well over 20 years and have brought up my 4 boys on my own, all while working as a secondary teacher. I still have two of them at home with me, while the oldest and the youngest have flown the nest.

I stumbled across the FIRE movement around 8 or 9 years ago by reading a blog called ‘Go Curry Cracker’. I remember asking him in the comments what this ‘FIRE’ acronym stood for. I was 49, I had just paid off the house and was worried about how I could ever possibly afford to retire.

Imagine my relief when I read the famous post by Mr Money Mustache about The Shockingly Simple Math Behind Early Retirement and I realised that by doing what I was already doing – (ie: saving and investing 50%+ of my take-home pay) I was on track to being able to retire at 67 with over a million dollar nest-egg. I could retire at pension age and not need to eke out my life on the pension.

That did it. I was hooked! I wanted to learn all I could about this FIRE stuff. I devoured blogs, books and podcasts. I hate Maths and numerals with a passion, but even someone as Maths-phobic as I am can learn, given enough repetition of the basic concepts.

Last year, at the age of 57, I retired. Ten years ahead of schedule.

I’m not your stereotypical ‘FIREy’ person, being older than a millennial, single with kids, coming from a career not really known for being lucrative and also being female. (And non-American…)

So what would I have said to the Money magazine people if they’d come knocking at my door? Here goes:

Frogdancer Jones* (* not her real name.)

Retired: at age 57.

Lives: beachside in suburban Melbourne with 2 of her 4 sons. Also with her 3 dogs who she possibly loves more than her children.

Career: Secondary teacher.

“I really believe that the secret to becoming financially independent is underpinned by three very important things,” says Frogdancer Jones as she pours a cheeky shiraz. “You have to know what you value in life so you can concentrate your time, effort and money on those things. You have to be able to see the value in delaying gratification – to be a long-term thinker, in other words. And you have to be willing to learn, so that when life offers up an opportunity, you can recognise it and – even more importantly, know what to do with it.”

The last point had a huge impact on the trajectory of Ms Jones’ financial life when, after years of struggling to bring up four boys and pay a mortgage on a teacher’s wage, she grabbed hold of an offer to develop her East Bentleigh property in a much sought-after school zone. This enabled her to release the equity in the property and move to a cheaper, but better, house further away from the CBD.

“Being able to pivot from my original plan to stay there until I was carried out in a pine box saved me having to work for an extra decade,” said Frogdancer. “I would never have had the courage to do it if I hadn’t have spent all of that time reading and listening to people who have already trodden the path to financial independence.”

So what does financial independence and early retirement mean to this early(ish) retiree?

“For me, the security of financial independence is an absolute gift. I left my husband back in 1997 with 4 boys under 5 and $60 cash. There were years of struggling to provide for my boys and pay the mortgage – it wasn’t easy to live off 18K/year of Centrelink benefits until the boys were all in school and I could go back to work. The frugal habits I learned back then have really paid off! If I have to, we can live off the smell of an oily rag. It took me a long time to lose the fear that I didn’t have ‘enough’ to retire on.

“Also, being able to retire at 57 is an even greater gift. For the first time in my life, I can be totally selfish. My kids are grown, I have no grandchildren and all I have to worry about looking after are the dogs and my garden. I can spend my days entirely as I choose – the freedom is absolutely incredible. I can highly recommend retirement!”

After starting to resurface after Christmas and New Year – so many naps! – I started to wonder what I might write that could interest people now that I’ve reached the goal post of every FIRE blog and actually retired.

There’s no point writing about what retired life actually feels like, because, to be honest, it doesn’t yet feel like I’ve retired. It’s the school holidays, my pay still keeps rolling in until the first day of term 1, so at the moment it still feels like business as usual. The 27th of January 2021 will be when it begins to hit home. The first school day of the year for teachers. My last pay packet ever…

But that’s still 3 weeks away. I started drafting this post yesterday but I wasn’t in the ‘zone’, but this morning I posted a comment about how I retired early(ish) on a teacher’s salary in a high cost of living city. It was in a Facebook group called Aussie FIRE discussion group, run by the guy behind Aussie Firebug. Someone replied, asking about my strategy.

I had to smile. My strategy?

Like most of us, I bumbled my way through my 20’s, 30’s and 40’s without a clue about FIRE (financial independence, retire early.) My only motivation, once I started manufacturing kids, was to provide a safe, secure life for them to grow up in. A lot of that was providing emotional security for them, but a huge part was also providing financial security. This involved things like ensuring that we always had a roof over our heads, enough food on the table and that the bills were always paid. When you leave your husband with 4 boys under 5 and $60 cash, which is otherwise known as the scariest financial decision of all, it tends to make you focus on the money stuff.

Although I didn’t stumble across the concept of FIRE until I was 50, the actions I took in the previous years accidentally set me up to be in a pretty good place to take the idea and run with it. Even though at that stage I’d just paid off my house, so my bank balance was literally $10 cash, I was primed and ready for the information.

So what enabled me to do the following: find out about FIRE when I had a paid-off house, around 100K in superannuation and $10 in the bank, and then to retire 7 years later?

A combination of the following behaviours:

The first tool, and undoubtedly the most important, was cutting my coat to fit my cloth. Otherwise known as spending less than I earned. Being frugal.

Frugality doesn’t mean being cheap – though in the early days when the boys were very young I’m sure I crossed that line a few times simply to survive. A frugal person makes sure that before they spend anything on lifestyle frills, they’ve paid the mortgage or rent, paid the bills and provided for the necessities of life. Then they tuck a little away for a rainy day in an emergency fund/investment portfolio. THEN they decide what to do with what’s left over.

The ‘decide’ in the previous sentence is very important. I feel that the main difference between a spendthrift and a frugal person is that one employs mainly short-term thinking with their everyday spending decisions, while the other employs mainly long-term thinking.

A person who deliberately decides to use frugal principles is sure to get ahead. I used to feel, especially in the early days, that every dollar I was able to keep in my wallet was a win. Those dollars I kept were able to be used to improve our quality of life on things I valued. These things are always a mix of looking to the future and enjoying the now.

Initially, those things I valued were chipping away at the mortgage, improving our car and house, paying for music lessons and sport for the kids and enabling the boys to see a little more of the world, both with family holidays and school trips. Then, as the boys grew older, getting out of debt, indulging in personal travel, (to the UK, Europe and North Korea – so far), and then investing for the future became the things I valued.

The trick with frugality is to spend only as much as you need to enjoy life now, while making damned sure you’re putting away money into appreciating assets so that you’ll be sure to enjoy life later – and not be a financial burden to your kids.

It’s a balance – I found that if Present Frogdancer put too much towards Future Frogdancer, it made me unhappy and discontented. But if I enjoyed a few simple pleasures in the here and now while continuing to look after Future Frogdancer, life became a joy.

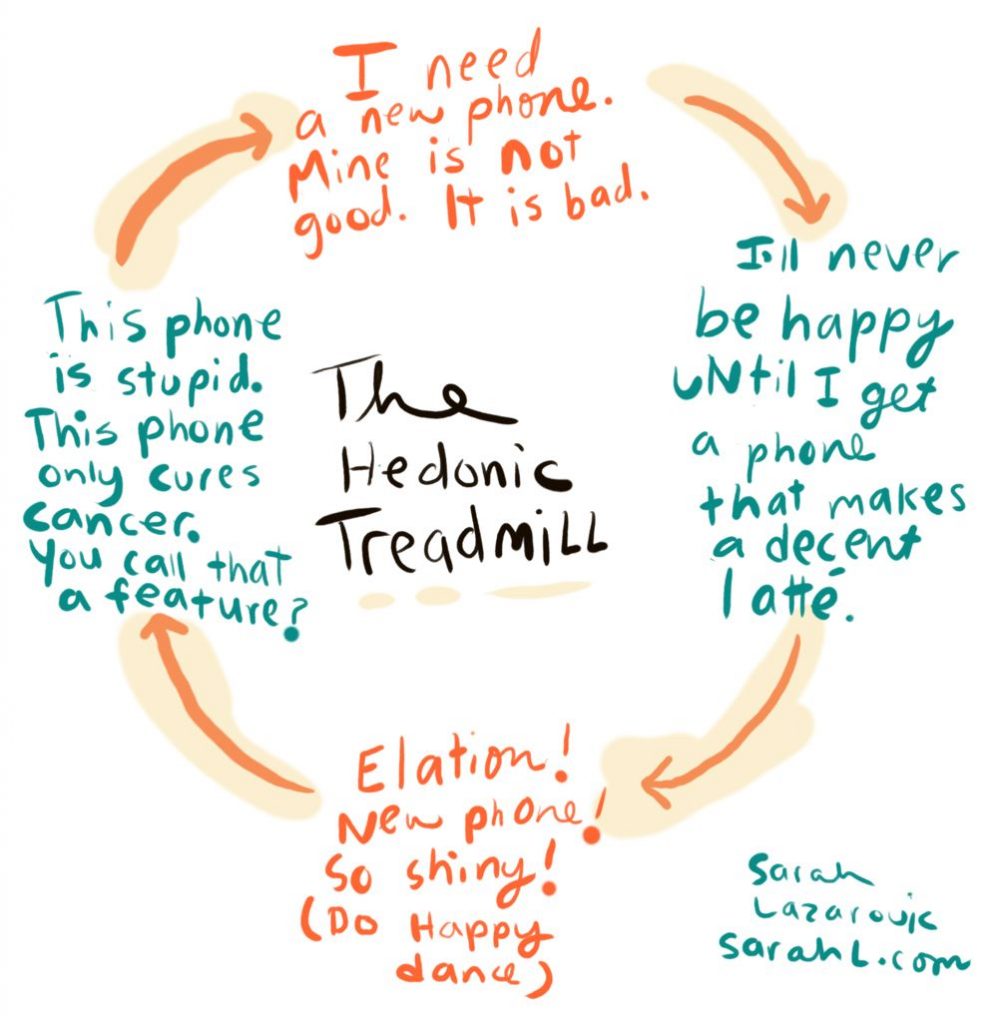

The second tool, which is closely linked to the first tool of frugality, is to recognise when hedonic adaptation, otherwise known as lifestyle creep, is threatening to happen. Then to make a conscious decision as to when, and how much, you let it affect you.

I first became aware of the term ‘hedonic adaptation’ during a Choose FI podcast when they were interviewing Barney Whiter, otherwise known as The Escape Artist. Basically, it’s when your spending increases as your income increases – at first you feel happy but then as time goes on you revert back to the happiness level you were before.

You know how it goes. You get a pay rise. You feel rich! You start getting takeout more often or going to restaurants more often, “because I can afford it.” You might upgrade the car, in order to drive something more befitting a person of your status. Clothes? Sure, upgrade the wardrobe! Get fancy furniture, buy some ski gear, buy a boat… you get the picture.

But over time, that new car doesn’t feel special anymore, it’s just your humdrum car. The boat isn’t a thrill anymore… in fact, it seems so dull and ordinary that you start to feel that you need a new one. The restaurant trips aren’t a treat anymore… they’re just a regular part of your Friday night routine. Humans tend to become used to new things over time and then crave what we perceive to be bigger and better things.

Your big pay rise doesn’t make you feel rich anymore. It’s a struggle to survive on such a small pay-packet. “No one can get ahead these days, it’s hard for the little man to survive.” You feel exactly the way you did before about your life, despite the new toys that initially brought you happiness. That’s the hedonic treadmill at work.

We live in a consumer-driven society. The trick is to only let your lifestyle increase by spending more on the things YOU value. Disregard what other people think that you should be buying. After all, they’re not going to be the ones helping you to retire early(ish!)

When I knew that I had a permanent position at my school, I took out a new mortgage to upgrade my kitchen, bathroom and the heating and cooling systems. I waited until I’d paid off that mortgage before I indulged in the overseas travel for myself that I’d always dreamed of. Could I have done both at the same time?

Yep. But I wouldn’t be retired now. Paying off that mortgage to become debt-free was crucial to becoming financially independent.

Recognising the temptations of lifestyle creep and deliberately choosing to limit your exposure to it means that you can pour your surplus money into assets that can increase your net worth over time. Again, it’s balancing the wants and needs of Present You vs Future You.

The third tool is looking to increase your income. The lucky ones are people who can negotiate pay rises in their day jobs. As a teacher in the government system, my pay was dependent on how many years I taught, so I looked elsewhere for ways to increase my income. When I became a thermomix consultant and team leader, I was able to deploy the extra money I made into paying off my house earlier and then paying cash for my decadent trip to the UK and Europe.

In other words, I used the extra money from my ‘side hustle’ to pay off an appreciating asset, (my home), and then used the excess funds to pay for a frivolous treat, (my trip), while all the while in the background the teaching job continued to pay for day to day expenses and investments for the future.

I did this for around 4 years. I worked my arse off between the two jobs and I was B-U-S-Y! And often very tired. But doing this turbo-charged my finances and put me in the perfect position to recognise the beauty of the FIRE concept when I discovered it.

The fourth tool is to be willing to learn.

A bit of background here: all my life I’ve avoided numerals and Maths. At school, I was in the top stream for English and at the same time, I was put into the veggie maths classes. When I see a page full of numbers my brain literally freezes and I can’t begin to work things out. I’m genuinely scared of them.

This is fine for an English teacher, but it’s not so great when it comes to learning things about the investing world.

My point is that, for me, it was HARD to start learning about how to invest. I’m sure it has taken me three times as long to understand about half what any normal person would learn in a given amount of time.

I was talking about this a year ago wth another English teacher who was asking for help with her finances. She said, “I wish it was as easy for me as it is for you, Frogdancer. I know nothing about this stuff.”

“It’s not easy for me at all!” I said. “My brain is like a rock and the information is like drips of water falling onto it. Over time, the drips make an impression, but it takes me longer than most to get it into my head.”

The tipping point for me was 3 weeks after I’d paid off my house. I’d spent three weeks buying ALL the yarn in every colour, brand new sandals, new clothes and I was happy. Then it dawned on me that you can’t eat your house. In other words, what was I going to do about retirement?

The thought of being in poverty scares me. I’ve been there, as anyone who’s read my ‘About’ page or heard my retirement speech would know. It was hard enough being young and being dirt poor – how much scarier would it be to be old and poor? I knew that the spending party was over. I had to start finding out what to do to put myself into a decent position by retirement age. In Australia, that’s 67 years old.

That gave me 17 years.

As luck would have it, the Barefoot Investor had just started an investment club, which has since closed. The first thing he put out was a ‘Rescue Your Retirement’ feature. After I read it, I literally cried tears of relief. My position wasn’t hopeless. There were ways to build a comfortable retirement for Future Frogdancer.

After that, I started reading. Books, blogs… I went down the rabbit hole. The relief I felt when I saw Mr Money Mustache’s post ‘The Shockingly Simple Math to Early Retirement’ and saw on his chart that if I saved 50% of my income I could retire in 17 years… omg. I was doing more than that already!

I just had to stay the course and I was probably going to be fine. I was on track to retire at 67 with a more than comfortable income. Phew! I could have stopped there.

But I kept on reading. The idea of having the freedom to do what I want in each and every day, unfettered by timetables, commutes and the demands of kids was beginning to intoxicate me.

I learned about different types of investments. Individual shares, LICs, ETFs, superannuation options, domestic and foreign geoarbitrage, property… you name it; I was reading about it. Like all learning, it started to open my mind to the possibilities…

Tool number 5, arguably as important as tool number 1:

ACT ON WHAT YOU’VE LEARNED, and be prepared to pivot if better information comes your way.

This sounds easy but in reality it’s really hard. No one likes the idea of losing money and making mistakes. But there’s a huge opportunity cost to sitting comfortably on your backside, deluding yourself into believing that because you’re reading about all this stuff, you’re ahead of over half the population.

You’re only ahead of the pack if you actually decide to DO SOMETHING with the information you’ve learned.

My first step was to move superannuation funds, first to the one that the Barefoot Investor recommends, but then when my friend The Mayor showed me that the default super fund in the same company actually gave far better returns, I swapped again. I pivoted slightly when better information came my way.

I began putting my savings into shares, index funds and LICs. Over time, it became my ‘shopping’ pastime. Some people shop for clothes, shoes and lattes; I shopped for shares. I looked don it as buying little scraps of my future freedom.

The brilliant thing about learning is that it opens the mind to opportunities that you might otherwise overlook. I learned about the concepts of geoarbitrage and property development, without ever thinking that I’d put them to use. Little did I know… if doing the thermomix side hustle turbo-charged my finances, utilising geoarbitrage and property development sent my finances screaming into outer space!

I wrote in detail about how I tweaked the geoarbitrage concept HERE. In the TL:DR version, I drew up plans to put 2 luxury townhouses on my house block in a desirable school district in Melbourne and moved 16 kms away to a far cheaper – but better- house 5 minutes away from the beach. By doing this, I freed up a TON of equity that was stored in that little house and shaved ten years from my working life.

This would never have happened if I’d been too scared to take the calculated risk and Just Do It.

When I think back to that 34 year old I wrote about in my ‘About’ page, sitting by the heater listening to the mice eating the bait and then I compare her situation to the one I’m living in now, the difference is enormous. I’m living the life that Past Frogdancer would never have even dreamed was possible.

It’d be too simplistic to say that the geoarbitrage decision was the one thing that brought all this to pass. It was certainly important, but I would never have been in a position to do it if not for the thousands of tiny little decisions I made along the way.

Frugality, living below my means no matter what, avoiding lifestyle creep, working to increase my income, learning about how to reach financial independence and then putting those concepts into action in ways that suited me and my family – all came together to bring me to this position.

I’m retired at 57. I can do whatever I want, whenever I want. I find that a very precious and beautiful idea and I’m looking forward to seeing how my life will unfold.

These tools aren’t the only dishes on the financial independence smorgasbord table. There are many more options and strategies available.

These are simply the ones that I used to get to where I am now. At first they were used for financial survival – then as time went on it morphed into working for financial freedom.

I hope that someone can take all of this and tweak a tool or two to use on their way to gaining their own financial freedom. The more, the merrier!

As of today, I have 108 days to go until I finish work for good.

Yes, I’m retiring.

My friend Scott suggested that I look at working days left, to make it seem even more delicious. Just counted it up. 47 working days to go.

On December 18 2020, Frogdancer Jones will be walking out of the classroom forever to go and live her best life. I’ll be 57 years old, exactly 10 years younger than the ‘traditional’ retirement age of 67 in Australia.

omg. I’ve bought back 10 years of my life.

I’m awash with excitement, anticipation and the tiniest dollop of trepidation. Its a big step, after all.

As you’re reeling back in shock, I hear you ask, “But how can this BE?”

Settle in. Here’s how it all happened:

In August an email went out to all of the staff, asking for our plans for next year. Did we intend to stay at the school, which subjects and year levels would we prefer to teach, would we be intending to take any time off etc. Without really thinking about it, I replied that I’d be working for another year at 3 days/week, just like this year.

In other words, force of habit. Inertia.

A week later, I mentioned to a friend, (let’s just call him ‘the Mayor’), that I’d signed on for another year. It was a conversation over Facebook. His reply?

“Another year. I’m a little surprised. I’ve noted your Covid-related comments and we certainly won’t have dealt with this by next year.”

Now the Mayor is the total opposite to me when it comes to a relationship with Maths. He loves analysing spreadsheets and company financials and everything like that. After my geoarbitrage deal finalised and I had the money from my house sale in my hands, he devised a spreadsheet projecting how my current investments could perform. I was so appreciative – it was a huge favour for him to do for me. So he knows my financial situation.

At the time that he drew up the spreadsheet, he said to me, “You know, you could retire now if you wanted.”

“NO WAY!!” I said. “I just don’t feel safe. “

He chuckled. “You can; you just don’t realise it yet.”

In the intervening years, I worked at making The Best House in Melbourne even BETTER – for Future Frogdancer Jones in retirement. I liked the idea of getting all of the expensive jobs over with while I still had a wage coming in. My post called ‘Why owning a home trumps renting‘ lists all the things I’ve put into this place, plus a few more that I’m thinking of.

After the Mayor’s remark about my Covid-related comments, I started thinking. Was it possible that I could actually retire?

I brought out the old spreadsheets and looked at them, comparing the projected figures with the real ones. I brought up my annual expenses chart, subtracting the costs of all the projects around the house that I’d been doing. I looked at how much I was spending to feed, house, clothe and shelter myself and the two boys I have still living with me.

That figure came in at just over 30K/year. Those meagre years have left their mark – I don’t waste any money on anything that I don’t value. My pleasures are either hellishly expensive (*cough cough Travel*) or are as close to being free that it doesn’t matter.

Hmmmm.

I contacted the Mayor again. Long story short, he’s preparing a document for me to take to a financial planner outlining everything to do with my finances, future plans and goals – all of that stuff.

Turns out I’m going to be fine.

But the clock was ticking at school. Kids were making their subject selections for next year and staffing decisions were being made. I didn’t want to jerk the admin around – getting my job at that school was the single biggest reason that I was able to dig the boys and I out of poverty. I owe the school a lot.

So, once I sat with the decision to leave for a few days and I still felt comfortable with it, I rang my boss.

“OH NO!!” was her reaction. But when we talked about the hows and whys of why I was leaving, there was nothing much else for her to say. She’s not stupid – she knew I’d made my mind up.

So why am I leaving? It’s not simply fear of getting Covid.

F U money.

FU money is a big part of it. After surviving the years at home with pre-school boys when we had hardly two cents to rub together, I’ve been hard at work ever since to do my best to ensure that we were never in that position again.

I’ve reached the position where I feel I have enough.

Enough.

I still love being in the classroom. The kids I teach are lovely and they’re so funny! It’s a rare day when I haven’t had a good laugh in class. I like the idea of going out while I’m still having fun – it’s much better than being ‘that teacher’ – the one who’s hanging on grimly to the job because s/he can’t afford to leave.

What’s getting me down is the insidious increase of admin. As one colleague said to me recently, “Honestly Frogdancer, it feels more and more that we’re becoming data collectors instead of educators.” We’re expected to measure kids’ performances all the time, with results put on tables and studies and projections – maybe the Maths/Science people like it but for me ? For me it’s sucking the soul and the fun from the job.

If I still had a mortgage to pay or debts to get rid of, I’d be staying. If I didn’t have enough to support myself on in retirement, I’d be staying. As I said, I don’t hate everything about the job. Most days are very pleasant days.

But there’s enough on the dark side to make me feel that now is the time for me to leave.

Fortunate Frogdancer strikes again! Going part-time this year, then having to spend months at home on lockdown has shown me that I have plenty of interests to fill my days. As long as the world contains books, the internet, Netflix and the dogs, there’ll never be an excuse to be bored. Spring has begun and soon I’ll be out planting seeds and designing my front yard. Yesterday I ordered $400 worth of fruit trees to plant there. There’ll be fruit to pick, cook and eat for decades to come.

I can’t see overseas travel being a thing for the next couple of years at least, but that won’t stop me planning for my trips back to the UK and Europe when things settle down. After all, I haven’t been to Windsor Castle to see Henry VIII’s tomb yet! Of course, there’ll be domestic travel as our internal borders open back up, so I’ll be well-placed to take advantage of that. (And I won’t have to wait for the school holidays when prices go up and everything is crowded!!)

Yes, it’s a big change. In one way I’ve moved quickly but in another way – I’ve been writing about retirement and financial independence for as long as this blog has been around, and I’ve been thinking and planning for it well before then! This decision has been years in the making.

I’m looking forward to what the next stage in my life will bring.

My house before I started working on the front garden.

Dave from Strong Money Australia wrote a post this morning about whether or not he and his wife should cash out their share portfolio and buy a house. I enjoyed reading it, as it’s the perpetual question with FIRE people who are good at Maths – is it better to invest in the share market and rent, or to buy a house and save on living costs down the road when it’s all paid off?

Me? I’m a home-owner through and through, not for any mathematical reasons (because Maths is hard) but purely because the security of having my own place that nobody can boss me around and kick me out of is too precious to give up. Also, having three dogs means that no landlord would rent to me anyway – and having the dogs is one thing that I will definitely not give up. So the freedom of home ownership is something that is integral to the Frogdancer Jones lifestyle.

When I bought my current house, I bought it with one eye to the view of the floorplan being perfect should any of the boys need to come back home after living away. Basically, the house is a rectangle divided into 2 main parts, so I can happily live in the front part while the boy/s have their privacy at the other end. The land was smaller than our original house, which was a plus because I was finding it hard to keep up with the upkeep at the old place. Also throw in that it’s just around the corner from an Aldi, 5 minutes walk to the dog beach and 4 minutes walk from the train station – the bones of this property are all great!

However, even though this house is pretty darned perfect, there have been things that I’ve decided to alter. Being in my mid-fifties, I know myself pretty week by now and there are some things that I know Future Frogdancer would love to have at her fingertips.

My plan is to get these things done while I still have a pay packet coming in so that I can cashflow some of the jobs, though in mid last year I took 40K in profits from my shares to kickstart the whole thing. I still have 20K left to spend.

I’ve spoken before about how 2020 was always going to be the year of getting The Best House in Melbourne retirement-ready for when Older Me/Future Frogdancer decides to stop teaching. The list of things I’ve done here since the money came through from the Domestic Geoarbitrage adventure is as follows:

Apple trees in the background. The back half of my yard is devoted to food growing.

Before we moved in I had the hardwood floors sanded and polished. Real timber floors were a ‘must-have’ and I enjoy looking at them every day.

Added a wall of cupboards to the laundry for my zombie apocalypse cupboard. It’s come in handy during lockdown! Also, put in some new cupboards in the kitchen, along with a fantastic wine glass storage feature. Easy access to wine is also a ‘must-have’!

Totally ripped out the backyard and landscaped it with old bricks – no more lawn mowing and no more weeds. I’m very lazy.

Installed 18m of wicking veggie gardens, plus a small ‘orchard’ of 5 apples, a pomegranate, an apricot and 2 limes.

Now I have to decide what to plant around my outdoor room so that it flowers in summer for Christmas.

Installed a whopping great verandah along the entire back of the house, creating an outdoor room for family get-togethers and parties. With 4 boys in their 20’s, I have a feeling that over the next decade or so the family is going to get larger!

Bought a teak table that extends to seat 12 for this new space.

Once our cats Daphne and Maris died, I bought brand new leather lounge suites to cut down on pet hair sticking to the furniture.

I also found a dining table and chairs, a tv cabinet, a couple of stools for the kitchen bench, an armchair for my room and a coffee table on Gumtree. These antique pieces are totally individual and will see me out. I love them and they were second hand, so they were far cheaper than new furniture of comparable quality.

My new front fence with my stellar painting. Now the dogs aren’t on guard duty all day.

We’ve put up a side fence between us and the new neighbours. They have a staffy who hates little dogs and both households definitely don’t want any bloodshed!

I wasn’t planning to replace the front fence as it was a metal picket fence and built to last, but the dogs kept barking every time they saw a dog go by. I figured if it was annoying me, it must be annoying the people around us. This new paling fence blocks the view and if it ever gets tagged by teenagers I can simply put another coat of paint over it.

If you look at the photo at the top of the page, you can see that there were two yucca trees on either side of the house. Whoever planted these next to walkways was clearly no brain surgeon. Every time I went to put something in the bin I’d nearly get my eyes poked out by the spiky leaves. These trees are now gone. I’ve bought a couple of avocado trees to take their place. I’ll be able to stand on the verandah to prune the trees and to pick the fruit. These trees have soft leaves so they’ll be a pleasure to brush past.

I live in a slightly dodgier neighbourhood than I used to. I put Crimsafe safety screens on all windows and doors.

I bought German-made appliances – I know they’ll be well built and will last far longer than cheaper ones.

When the people before us did up the place to sell, they installed the cheapest stainless steel appliances that they could. It was on my list to replace them ‘someday’… but during lockdown the oven and dishwasher both died, so it seems that my kitchen renovation is suddenly pretty much done!

When our hot water service died I replaced it with a continuous gas hot water service. Expensive to set up, but over time it saves on gas and as an added bonus, people can program their showers to be the exact temperature that they want. I like this little luxury!

When a friend at work told me that her husband worked at the Reece plumbing ‘samples and seconds’ shop, I ducked in and bought all the fixings for my new ensuite I’ll have installed one day. I saved at least 8K on what I bought because he gave me mates rates on top of the already cheap prices. At the moment it’s all in boxes and bubble wrap cluttering up the boys’ lounge room, but that’s ok in the short term.

Astute readers will have noticed that few of these renovations are what people would consider “essential.” We could have moved into this place and lived quite happily without the brick paving, the new cupboards and the polished floors etc. After all, the families who lived here before us did just that.

But owning this home means that I can tailor it to the way I want to live. For example, I enjoy growing some of our food. To me, having literally half the backyard set aside for this is a great use of the space. But I don’t want to have to mow a lawn or weed all the time, so spending money on paving makes me happy, as I know I’ve freed up Future Frogdancer’s time. I don’t want her to fall down and break a hip trying to pull up a weed in about 30 years time! I could have put concrete down at a fraction of the price of the bricks, but I like the natural look of the bricks, so again – money well spent.

Scout. She’ll be 4 next month – where does the time go?

I value a calm, peaceful home without any troubles from the council and the neighbours. The fencing I’ve put up isn’t the most exciting way to spend money, but it’s worth it because it keeps Poppy, Jeff and Scout safe, secure and QUIET.

I’m basically thinking about the things I like to do and the values I want to live my life by and then seeing how I can design my home to include as many of these things as possible. I want to have Future Frogdancer fit into this house like a happy little pea in a pod.

So remember I said I still have 20K left? I feel like a bit of an idiot because I had one job that absolutely needed to be done, but I kept putting it off because I was scared about how much it would cost.

Yeah… this doesn’t look good…

My front verandah has timber balustrading that has seen better days. I had absolutely no idea how much it would cost and then with coronavirus coming along, I shoved it into the back of my mind and tried to stop thinking about it.

Except… this job was only going to get worse with time and turn into something that would just get more and more expensive the longer I ignored it. So, after a year of resolutely turning my face away from it, I called in a couple of tradies to quote.

ARGH! I’m such a fool! I thought it’d cost thousands! I got the first quote back last night – $1,040. I could have had this done AGES ago. I’ve been needing to get this done so I could then plant my avocado trees. They’re still in their little pots, instead of getting their feet in the ground and producing those smashed avos that my millennial boys dream about.

As part of this job, I’m also getting a piece of laserlight nailed to the underside of the verandah, where an access door is. This will be where I’ll put our lawnmower. It’ll be tucked away out of sight, safe from any rain and it’ll be right where the lawn is – no wrestling it down from the backyard. Again – I’ll be getting something done that suits me.

So what else is on my list?

The other side fence. It’s literally falling apart, so once I get this done I won’t have to worry about fencing for decades.

Beautifying the new back verandah. I’ve bought the dining table and chairs and we have an old couch there, but it needs plants around the perimeter and I want to get a couple of half wine barrels to put splashes of colour in. I also want some sort of artwork on the wall of the house to make it all look pretty.

A new ensuite. My old one is perfectly serviceable, but it has a shower over a bath. I HATE THIS – it’s so pov. Plus I think it’ll be unsafe when Future Frogdancer will be getting in and out of it – one slip and she’ll be in a world of trouble.

A Tesla power wall. I don’t know if I’ll be able to get one of these, but I’d love it if I could. I’m looking for ways to future-proof Future Frogdancer’s bills and seeing as I already have solar panels, this could dovetail in quite nicely. Plus, I like the idea of having a back-up when power cuts and brownouts happen during the summers. I have a niggling feeling that these will get worse as time goes on and peak oil starts to bite and I don’t want to suffer through hot temperatures or have my freezer lose all of its contents. I freeze A LOT of things, particularly from the garden and I’d be incandescent with rage if I had to throw it all out.

An office/crafting room. OMG. I’ve never had one of these in my life and I’d love one. When we looked at this place, one of the back bedrooms was set up as an office. It has a door through to the backyard and it has a wall of cupboard save lined with shelves. THIS is the space. Unfortunately, Ryan25 lives in here and he’s not going anyplace soon – he’s finishing his remedial massage course and going straight into a 12-month myotherapy course. So this one will have to wait. But when I have all of my paperwork, my sewing machine, my yarn and my fabric all organised in the one room, I’ll be a very happy woman.

Painting the inside of the house. This isn’t urgent, but like the kitchen fittings, the previous owners did a very quick spray job. I’d like enamel paint on the skirting and doors, instead of the matt paint I currently have. It’s impossible to wipe down properly.

Landscaping the front yard. I have a vision of people coming through the high front gate and being greeted with a beautiful oasis of flowers, fruit trees and lawn that is invisible from the street. Apart from my avocados, I have absolutely no clue what I’ll be planting here. None whatsoever. But it’ll come to me.

The beauty of having my own place is that once I set it up, I’ll be able to live here with minimal ongoing costs and I’ll be perfectly happy with everything I have around me. I plan to travel overseas every year (once this pesky pandemic sorts itself out) but when I’m at home, my dogs, my crafts, my books, my blogging and my gardening will occupy me very nicely.

Once you buy furniture, that expense goes away as you have it for YEARS. Given this, it’s worth it to hunt around for items that really suit you. I found this out the hard way. When I moved in with my boyfriend back in the day, we bought some ugly cheap pine furniture “just for now”. A marriage, divorce, 4 kids and twenty years later, I finally got rid of those eyesores. It’s better to buy things you love looking at (like my bedroom setting that I’ve had for 25 years and have no plans to replace), because furniture hangs around for decades. My rule now is to allow nothing through the door that I don’t love, no matter how “practical” that thing may be.

One of my propaganda posters from my trip to North Korea, along with a North Korean banknote that I smuggled out.

My plan, once the world opens up again, is to gradually fill my walls with paintings and drawings from places that I’ve visited. I’m in no hurry to fill the empty walls I have. I’ll see something on my travels and know that I’ll want to look at it for the rest of my life and it’ll find its way home.

I love the idea of slowly building a collection of art that will spark memories of my travels and will make my house look totally different to anyone else’s. My house will reflect ME. So far we have Balinese paintings, pieces from North Korea and Venice and France. I wonder what else will join them as time goes on?

I save vegetable seeds and grow from them year after year. I love the idea of feeding myself and my boys food that started from seeds I bought years ago, but which still feed and nourish us years into the future. There’s something about the continuity and the tradition that appeals to me.

Home ownership is something that is definitely a financial struggle in the beginning. Homes are not something that vendors just casually give away! But over time, as the mortgage is paid off and there’s extra money available, there’s a beautiful opportunity to craft your living space into the perfect space for YOU.

Being on the FI/RE path as we are, the vision of decades of freedom in a space we simply enjoy living in is something to be aimed for. At the moment I’m having the fun of planning and ticking tasks off the list one by one. In a couple of years, I’ll have the fun of actually spending huge gobs of time in this home I’ve created. A home that keeps costs to a minimum. A home that makes me happy and fulfils my needs.

While I’m stuck here at work, putting in my last day before the winter holidays, please duck across and have a read of this series. There’s some very interesting and determined people there, who all prove that you can still retire early, even if you don’t discover FIRE until your 40’s or 50’s.

I’m always interested when retired people continue writing their blogs, or when people post interviews with people who have already reached early(ish) retirement. So many of us in this space are still working our way towards the time when we can strap on our socks and sandals and skip off towards the sunset, so it gives me great motivation to hear from people who have reached the goal and can let us know what it’s like to live the dream.

Today I have a post from my best friend Blogless Sandy. She and her husband retired a couple of years ago, long enough to settle into it, so I thought it’d be interesting to hear her perspective on this whole retirement thing. The photos she’s attached also means we can literally see her perspective as well!

Here she is:

After a lazy mid-week lunch at a winery.

I’m Blogless Sandy, aptly named by Frogdancer because my real name is

Sandy and I don’t have a blog. Who would have thought an English teacher could

be so imaginative!

Anyway, given that Frogdancer is working her way towards retirement and I’m already there, she has asked me to write about my experience of retirement so far, a whole 2½ years of it. This all started after her post quite while back titled “Retire? But what will you DO all day?” and a discussion we had at the time about retirement in general. Frogdancer and I met 24 years ago when our kids were still babies and we’ve remained best friends ever since, so we discuss stuff a lot.

A little bit about me. I’m married with 2 adult children and 2 grandchildren. My husband and I retired to the Mornington Peninsula (about an hour from Melbourne, Australia) 2½ years ago, after selling our large family home in a suburb of Melbourne. My husband, who is 11 years older than me, had just retired. Selling our home and buying a smaller house further from the city meant I could also retire immediately. I was 56, so although not an early retirement by FIRE standards, it was still a lot earlier than most Australians manage.

Blogless Sandy, like me, has a dog beach at the end of her street. How handy!

I retired on a Thursday and we moved to our new home (the best house on

the Mornington Peninsula) the following Monday. When I look back I contemplate

that it could have been a complete disaster. I left our family home of 24

years, my job of 27 years, our friends and everything that was familiar, moved

to a totally new location, and all within the space of 4 days. Was I concerned?

Not at all… well, if I’m being totally honest, maybe just a little bit.

When I announced to friends and work colleagues that I was retiring and moving, the question asked most often was “But what are you going to do?” I’d never considered that filling my days was going to be a problem, but it seemed to be a concern for others. This is understandable, given we spend a good deal of our lives in the workforce with our schedule dictated by our job. Then when we are at home, for many, much of the time is taken up with raising a family and running a house. Our lives are interspersed with holidays where we get to choose what we want to do, but trying to imagine a life that is essentially one big extended holiday can be difficult.

For me, the biggest change when I retired, apart from the obvious one of not having to work anymore, was the lack of social interaction compared to working in an office environment 4 days a week. Even though we often work with people that we are not necessarily friends with outside work, we tend to socialise quite a bit at work. We usually talk with work colleagues about our weekends, events we go to, activities we participate in and just make comments about things in general. Suddenly all that was gone! It was just me and hubby! But don’t panic, it all worked out fine, without one of us doing serious harm to the other. Just saying though, it was a huge change that I hadn’t really thought about before it happened.

Fortunately for us, we’re both reasonably self-contained people who are quite happy with our own and each other’s company. For people who struggle a little with the whole being on your own thing though, it’s probably worth considering how this will impact you. You might surprise yourself and learn to love all that “aloneness”. You may discover that you’re actually damned good company and that a bit of alone time can be quite replenishing.

Just another afternoon at the office on the beach.

I liked Frogdancer’s post (mentioned above) as she was obviously considering that retirement is not just about travel and sleeping in. The day to day needs to be filled with something too and having a number of projects or interests in mind is a good start. When people asked me what I was going to do in retirement, my response was that for the first 6 months I would sleep, read, knit, take long walks along the beach, spend time with my grandchildren and explore our new location. Then once I got bored with that I would consider what else I wanted to do. Of course, I had projects and activities in mind, but my initial goal was to just unwind and treat the first stage of my retirement as an extended “staycation”. I picked 6 months as an arbitrary length of time, not really knowing if it would take more or less time before the boredom began to set in.

Imagine retiring early enough so you can keep up with a toddler?

And there’s that word – boredom – that we all seem to be so afraid of. Now I agree that an extended period of boredom is not a good thing, but I don’t believe that short periods of boredom are all bad. After all, if you’re a bit bored, isn’t that when you start looking for something to do? I know in my life, many a good project or new activity has been kick-started by a little bit of boredom.

One by-product of retirement is that I’ve finally learned to slow down – most of the time anyway. It took quite a while to wind back to a gentler pace, but generally I no longer feel the urgency to get everything done today, not when I can see a whole bunch of ‘todays’ in front of me. Life is not lived at the same frantic pace as before and there is more time to enjoy the small moments. Interestingly too, having learned to slow down, I just don’t need as many things to fill the day. Compared to my pre-retirement life, I now feel like I do a lot of “nothing”. It’s not really that I’m doing nothing of course, but I’m going at a slower pace and enjoying more quiet moments.

Being able to spend more time with the dogs – sounds good.

I know that before I retired, I generally thought of retirement as a

fixed kind of thing. You retire, you do certain things, lead a certain kind of

life and that’s it until you’re carried out in a box. I realise now, that for

me at least, retirement is more of an evolving process. Initial retirement was

the “relax and unwind” phase. After years of raising a family and being in the

workforce that’s what I needed. There were lots of sleep-ins and idle mornings,

lots of lazing around. There were lots of days with nothing planned and lots of

spur of the moment outings. It was wonderful, but I reached a point where I

needed more than that. I’m the kind of person who functions better when I have

some kind of structure to my week and that’s what I have now.

I like the sameness of familiar activities and pastimes, but I also revel in the challenge of doing new things too. Now, 2½ years into retirement I find I’m busy, but a new kind of busy. I’m busy doing the things that I want to do. I always said that when I retired I wanted to volunteer at an animal shelter, so now I walk the dogs at a shelter one morning a week.

Taking a hike on a mid-morning Thursday.

I also participate in a walking group one morning each week, always in a different, but nearby location. I get exercise and social interaction and get to explore the local area, all in one activity. We look after our grandchildren 1 or 2 days a week, but that has become fixed days rather than the casual arrangement it started out as. I prefer the fixed arrangement as it fills my need for structure.

Imagine having yoga classes in a studio with this outlook?

I always used to speak about doing yoga or pilates but had never actually done more than talk about it. I no longer had the excuse of being time-poor, so I took up yoga about 15 months ago and currently attend 5 classes a week. Then there’s the small commitment of being a member of the local beach cleaning group and trying to combat the never-ending amount of rubbish that gets left behind or washed up on our local beach. In amongst these things are the outings, the dog walking, the bike rides, the walks along the beach, the catching up with friends, the gardening and the pottering around. Oh, and just a bit of bad news, even in retirement the housework still needs to be done!

It’s a lovely kind of life that I’ve created and I’m very content.

That’s not to say things can’t or won’t continue to change though. I feel free

to keep creating the kind of retirement I want and as time goes on circumstances

are bound to keep changing. We were only recently contemplating that before we

know it our caring commitment to our grandchildren will be reduced to just

school drops-offs and pick-ups. Then we found out that grandchild number 3 is

on the way!

Little do they know they’ll have company soon…

I spent 12 months volunteering at 2 animal shelters and recently decided to discontinue one of the roles. I was feeling overcommitted (overcommitted in retirement! haha!!) and my role at one of the shelters was very physical and rather thankless. I kept going for the sake of the animals, but ultimately decided to focus my energy on the shelter where I feel my contribution has the most impact and is more valued. If I want to increase my shelter volunteer work again in the future I can easily commit to additional shifts at that same shelter.

As mentioned, I took up yoga about 15 months ago. I was attending

classes once or twice a week and decided about 5 months ago to make a bigger

commitment. I didn’t feel I was doing my yoga practice justice and wanted to

see how I’d feel about the whole yoga thing if I got a bit more serious about

it. So now I attend 5 classes a week and yoga is my current obsession!

After another 2½ years of retirement, my weeks may be entirely different. I may decide in the future that I want more in my weeks, less in my weeks, different or new things in my weeks. The beauty of retirement is that it’s an evolving process full of endless possibilities, limited only by what I want it to be.

So don’t be concerned when people ask you what you’re going to do in retirement and you don’t have all the answers. If you have a vague idea of some things you want to do and some interests you might want to explore, you will be able to create the perfect retirement for you.

Retirement looks awful, doesn’t it?

It’s me, Frogdancer Jones again!

I really like how Sandy and her husband utilised domestic geoarbitrage in much the same way I did to free up capital that was otherwise locked into real estate. Being able to use that money to downsize and invest has shaved YEARS off her working life (and mine too! It’s 2020 – hello part-time work!!)

Something that she didn’t touch upon is that retirement looks a bit different for her and her ‘hubby’. Blogless Sandy likes a structure to her week, whereas her husband is a more ‘go with the flow’ person who takes each day as it comes.

For me, looking at how they’ve settled into their new life down on the Peninsula, it’s made early(ish) retirement seem far less risky and scary. They live life in their own ways and they’re very happy. I could do with a piece of that…

Thanks, Blogless Sandy. Enjoy your beach and your spa!

I guess I’ve always been a bit of a saver. When I was in my teens and twenties I’d willingly save whenever I had a goal in mind, but if I didn’t, I’d tend to drift along the path of life, buying what made me happy in the moment. Heck, in my 20’s I had a VERY expensive dog breeding and showing hobby, which sucked up thousands of dollars over the time I did it. Poppy and Jeff are the descendants of that breeding program, so I’m very glad I did it!

Back in those days, I had no thought for an emergency fund, as I was living with my boyfriend/fiance who had his own small business. In those early days, money wasn’t a problem. It was predominately a cash business. When his accountant asked if he wanted to pay tax on his earnings and A said no, the accountant told him to “Piss it all up against the wall then!”

Dimly, this worried me. It seemed like such a waste. But I told myself it wasn’t my business and it was A’s money, not mine. However, things change. By the time we were married some stiff competition had moved into the town we were living in and the financial good times began to slip away.

Ten years later, by the time I walked out, our finances were dire. By that stage, we had 4 boys under 5, a house with a mortgage just under 100K, two very old and worthless cars and $60 cash each.

Obviously it was easier for my ex to move out of the family home and for the boys and me to stay put while we tried to work out what was going to come next. I allowed him to stay for 6 weeks to get some money together while I slept on the couch. I’m short, but even so, it wasn’t the comfiest of beds! After 6 weeks I asked him when he was moving out and he said, “I haven’t arranged anything. I thought you’d change your mind by now. ” After being informed in a fairly direct way that no, I needed time apart to see if there was anything left of the marriage to save, he borrowed some money from his sister and moved out a couple of days later.

My ex had no money and very little cash-flow from his business, so in lieu of any child support, he agreed to keep paying the mortgage. Meanwhile, I went on what was then called the “Sole Parents’ Pension’, which gave me around $300/week to support the boys.

I felt extremely vulnerable. Every time I looked at the boys I grew more and more determined that they wouldn’t suffer for the mistakes that I’d made in some of my life choices.

I knew I needed some cash to stand between us and a cruel, hard world. I hadn’t heard of an ‘Emergency Fund’ then, so in my head I called it a “Buffer Zone” I decided a thousand dollars would make me feel safer. It seemed like an insurmountable sum to find, but I knew I had to try.

So I started saving. The next 3 months were TIGHT. Every bill was paid as soon as it entered the house and I scrimped and scraped on everything else. If we had a meat meal, the boys had all the meat and I lived on eggs and veggies. Sometimes, if I was really desperate, I’d cut the end off a sausage and devour it. I felt guilty, but sometimes smelling those snags cooking was more than flesh and blood could stand!

The boys’ protein came from mince, sausages, tins of tuna and eggs. We didn’t waste an ounce of food. Funny thing is, some of the meals I made over this time have morphed into our family’s comfort foods. Scotch oatcakes, tuna mornay, cauliflower + macaroni cheese… funny how desperation can turn into fond dinner requests!

At around the 3 month mark I’d saved the one thousand dollars. I breathed a sigh of relief and felt a glimmer of pride. I’d done it! We were safe! But then a little niggle of something made me decide to call the bank to check on how the mortgage was going…

“I’m sorry Mrs ******, but your mortgage is $968 in arrears,” said the nice bank man on the end of the phone. I nearly dropped the receiver. How could this be possible? A said he’d pay the mortgage. It was supposed to be his way of supporting his own children, for God’s sake!!!

My first reaction was disbelief. Then it was blinding anger. How could he recklessly put the boys’ security at stake like that?

My third reaction was a mix of resignation and relief when I thought of the Buffer Zone money. It’d cover the arrears. I loaded the boys up into the double stroller and took a walk down to the bank. Within half an hour of that phone call, our account was back where it should be and I now had around $30 to my name. Half what I walked away with 3 months ago when I left my husband. But the house was safe, which meant so were the boys.

If that doesn’t bring home to a person how important it is to have an emergency fund, then I guess nothing will. If I didn’t have that money put aside and the bill for the mortgage got worse and worse, the trajectory of how our lives turned out would have been vastly different.

That little house was the place we lived in for the next 20-odd years, after I bought my ex out in the property settlement a year later. It was in one of the best public school zones in Melbourne and so my boys got a great education. As an unexpected bonus, I’ve been working at the same school for the last 16 years and so my little family ended up having a stable income, no matter what A decided to do with child support. And in 2018, the sale of that little house enabled me to utilise Geoarbitrage in the same city and release a tonne of equity which has probably saved me from a decade of having to work.

As soon as the boys and I walked back from the bank all those years ago, I started building up that Emergency Fund again. When I was at home with them, before Evan, my youngest, started school, my Buffer Zone was 1K. We had to use it a lot as things cropped up, sometimes the Emergency Fund would be depleted and I’d be reminded yet again about how essential it was to have money put away. You just have to read my ‘About‘ page to see that!

However as the years rolled on and I was in a secure job, as the level of cash in the Emergency Find rose, so did the likelihood of me having to tap it. It’s strange how that works.

A few months ago I had to tap it for the first time in years. Our hot water service blew up and I wanted to replace it with a gas continuous hot water service. What could have been a financial drama was just a minor inconvenience, because I had the money on hand to pay for it. I’m in the process of building it back up now.

Sometimes I see posts stating that the need for an emergency fund is overstated and that people would be better off putting that money into the share market and letting it ride. That’s pure stupidity in my opinion. Having a few grand put aside in an online high-interest account that you don’t touch unless something totally unexpected comes up – this won’t slow you down towards your march towards financial independence! Think about it. We’re looking to amass hundreds of thousands of dollars. Ten grand or so in a savings account is a drop in the bucket compared with that.

I woke up this morning to the news that the ‘Playing With Fire’ doco is coming to Melbourne. Naturally I booked a ticket right away.

The link is HERE. Camberwell’s a fair hike from where I live, but I figure I can always take the next day off – I’m trying to use up my sick days before I pull the pin on the job anyway!

Normally, you don’t get a window into how other people may see you, but last week I did. It was pretty confronting, to be honest. It actually stopped me blogging, while I mulled over it.

I’ve known Fred and Wilma pretty much all my life. They’re old friends of the family and, now that I’ve changed the way I drive home each night, I drop in on them occasionally.

Anyway, I was visiting Fred and Wilma after work one night last week and having a cuppa and a chat. We were talking about their family and mine and just generally catching up on what’s been going on.

We’d been talking about money matters a few minutes before. Fred and I share a similar interest, so I told them about a financial goal I’d achieved. Then the conversation moved on, as it does. Coincidentally, Wilma had talked with my sister a day before and she shared a story about a win that my sister had. Kate’s a Thermomix consultant and she did a demo at a gorgeous Bed And Breakfast place in the country – and ended up being able to stay there that night for nothing. She had a lovely time.

“Looks like being a good week for the Jones girls,” I said. “We’ve both had wins.”

“Yes, but yours are only ever about money,” replied Wilma.

Wait… what?!?

Yeeouch!

This has been reverberating around my head ever since she sad it. At the time I made some sort of verbal come-back, but it was pretty feeble, as she’d well and truly caught me on the back foot.

I’m still not sure exactly what she meant by it, though I have a sneaking suspicion that me still being single, 22 years after I left my husband, might have a bit to do with it. I don’t think it can be the boys – no one’s in jail, on drugs or living on the street. All of them have either finished University or are well on the way to.

I’ve held down a full-time job for the last 15/16 years – I’m never quite sure how long I’ve been at the school – and I’m pretty sure I’m good at what I do. After all, I’m changing lives… one English or Theatre Studies lesson at a time.

It’s a weird thought to think that just when I’m closer than ever to reaching my goal of early(ish) retirement and I’m stepping back from a six-figure wage, I’m being called on for being too mercenary.

The thing is… I don’t think I measure my life’s success simply by how big my net worth is. Sure, it’s a part of it, because I’ve worked too hard and planned too much for it not to be. But I’m investing and planning so that all the intangibles in my life will be easier – things like the freedom to spend my time how I choose; the ability to help anyone I feel like; the choice to share things like theatre tickets and other fun things with the people I care about and the ability to go traveling any time I want.

Ok, so maybe that first and last ones on the list might appear a bit selfish, but so be it! I bought a beautiful house three years ago when I did the whole geoarbitrage gamble, but part of the decision to buy this place was that the layout of the space meant that when the boys want to move back for any reason, we won’t be living cheek to jowl with each other. Part of my job as a parent is to provide a roof over their heads and I feel glad that I can provide it if they need it, even though they’re all adults now.

Doesn’t mean I still don’t love my house. Doesn’t mean I still don’t think it’s beautiful. But it’s an example of the way I make decisions – there’s often a long-term plan behind the spending/life decisions I make.

It’s an interesting question though – money is behind a lot of the decisions, obligations and freedoms we have in life. It’s obviously important. We in the Personal Finance and FI/RE blogging communities write about it all the time.

But Wilma’s perception of me rocked me back on my heels a bit. It makes me wonder. Is she alone in her view of how I view success, or do others feel the same?

Of course, short of asking everyone I know, I’ll never get the answer to that curly question! But it was interesting to have that little window into how someone else perceives me.

I guess it does you good to get the wind knocked out of your sails every once in a while, to stop you getting complacent.

I’ll still drop in every now and then to see Fred and Wilma, but I wouldn’t be surprised if Fred and I have our little financial chats in private from now on…

Many novels have basic money lessons woven through them, which is understandable really. After all, money is integral to the human condition, which is what literature is all about. Few novels, however, concern themselves with money lessons so much as Pearl S Buck’s ‘The Good Earth.’

For those who haven’t come across it, this is a cracking good read. It covers the story of Wang Lung, a poor Chinese peasant eking out a living on a farm in the days before Communist rule. Wang Lung is poor… dirt poor. But he has ambition and a fierce love of the land. This novel traces his life as he rises from poor peasant to rich landowner and what happens to his character and family along the way.

All images are taken from the 1937 film of the same name.

Wang Lung’s wife is chosen for him by his father. A practical man, his father chooses a slave girl from the rich and powerful House of Hwang in the village, a girl who can work hard on the farm as she doesn’t have bound feet, much to Wang Lung’s disappointment.O-Lan is not a beautiful girl, but she is devoted to the farm and to her new family and there is much more to her than meets the eye.

Of necessity, the family is frugal. I first read ‘The Good Earth’ when I was a teen and to this day, I still have to get every grain of rice out of the cooking dish, exactly as O-Lan did. I think of her every time.

They waste nothing. At first, it’s from mere survival instinct, but as time goes on and O-Lan’s skills bring more prosperity to the family, they begin to buy land. In their society, land was the only thing that could buy security and prosperity. This was especially important to them as their family started to grow.

O-Lan goes back to visit the House of Hwang with her first baby, dressed beautifully. The Hwang family clearly need to read ‘The Millionaire Next Door’. She says to Wang Lung:

“I had but a moment for private talk with the cook under whom I worked before, but she said, ‘This house cannot stand forever with all the young lords, five of them, spending money like waste water in foreign parts and sending home woman after woman as they weary of them, and the Old Lord living at home adding a concubine or two each year, and the Old Mistress eating enough opium every day to fill two shoes with gold.’ “

However, no bull run in the stock market lasts forever and it’s the same with life on the land. A few years later famine strikes. Despite having resources tucked away, hungry relatives descend upon them demanding to be fed and soon Wang Lung and O-Lan’s ’emergency fund’ of food and money is gone.

The neighbours didn’t know this and, fired up by Wang Lung’s evil uncle, they descend on the house and strip it bare, looking for food and other items of value to steal. There was nothing but a few handfuls of beans. After they leave, Wang Lung comforts himself with the thought that he’d put all of their spare money into investments, which in his case was land:

“They cannot take the land from me. The labour of my body and the fruit of the fields I have put into that which cannot be taken away. If I had the silver, they would have taken it. If I had bought [food] with the silver to store it, they would have taken it all. I have the land still, and it is mine.”

The lesson here is clear. If you store your net worth in things that cannot be seen, you have a better chance of preserving them when things go wrong. Anyone can run away with a bag of diamonds or a shiny new car, but a share portfolio or a fat superannuation account is easy to hide.

Back then in pre-communist China, of course, there were no unemployment benefits. You either starved when the food ran out, or you found a way to make some money. Or you practise geoarbitrage and move to where things are better.

The family sell every stick of furniture in the house, except for their farm implements, and they set off to a big city 100 miles to the south, where the famine hasn’t reached. Geoarbitrage! Wang Lung picks up work pulling a rickshaw, while O-Lan and the children turn to begging. O-Lan utilised skills she picked up as a child to show the others how to make money as a beggar. One should never forget skills that one picks up along the way!

An easy way to make money was to sell a child to a rich family. O-Lan revealed that this was how she herself had become a slave. The couple had two sons and an infant daughter by this time. No way would they part with the sons, but the daughter? Wang Lung decides not to sell her, but it was a close thing.

Sometimes the road to financial independence relies on seeing an opportunity and taking action. While the family is stuck in the city, with no way to earn enough to get back home, there is some sort of revolution and the rich homes are looted. Wang Lung is borne along by the crowd and takes nothing, however O-Lan, who has lived in a Big House and knows what to look for, finds a cache of jewels.

The family is now set! They travel back home, with enough money to buy lots of land and set themselves up for life. O-Lan requests that she keep only 2 small pearls from the jewels.

‘If I could have two,’ she went on humbly, ‘only two small ones—two small white pearls even… ‘Pearls!’ he repeated, agape. ‘I would keep them—I would not wear them,’ she said, ‘only keep them.’

The rest they use to buy land from the House of Hwang where O-Lan once lived. That family has now fallen into decline, due to opium addiction and general financial recklessness.

There is now money enough to employ others to work on the land, money enough to take the sons from the fields and educate them and money enough to support some leisure activities. Wang Lung eventually buys the House of Hwang’s residence and moves his family in. To think! What was once the pinnacle of wealth and power to him, is now his.

However, lifestyle creep starts to cause problems.

O-Lan continues on as usual, but Wang Lung falls prey to peer group pressure from other rich men and starts going to gambling dens and ‘tea houses’. This is where he meets Lotus, a lady of the night. She looks like a kitten, with the smallest bound feet Wang Lung has ever seen.

She is incredibly beautiful, totally greedy and selfish and she bedazzles Wang Lung. He showers her with money and even asks O-Lan to give him the 2 pearls she had kept from the cache of jewels, so that he could give them to Lotus. After a while he couldn’t bear the thought of other men sleeping with her, so he buys her from the Tea House and brings her home.

He builds her an inner court where she lives with her own household, so she and O-Lan don’t have to see each other. O-Lan is now totally disregarded by Wang Lung as she quietly goes about doing her regular work for the family until her death.

As the family gets older, lifestyle creep continues to happen. But through it all, even as silver streams from their hands, Wang Lung will never sell any of the land he has accumulated. He knows that it’s the bedrock of their fortunes and everything else they’ve managed to build and to buy is based on that.

He’s the definition of first-generation FIRE. But unfortunately, he was so focused on his work, what the rich men of the town thought and on Lotus that he made a huge mistake. The next generation had been allowed to grow up without having much contact with the very thing that had given them their prosperity. They could remember nothing but ease and comfort.

At the end of his life, he is living back on the original farm with his daughter and a concubine. He overhears his two sons talking about how they will divide the estate once Wang Lung has died, which fields they will keep and which ones they will sell:

But the old man heard only these words, “sell the land”, and he cried out and he could not keep his voice from breaking and trembling with his anger, “Now, evil, idle sons – sell the land!” He choked and would have fallen, and they caught him and held him up and he began to weep.

Then they soothed him and they said, soothing him, ” No – no- we will never sell the land – “

“It is the end of a family when – they begin to sell the land,” he said brokenly. “Out of the land we came and into it we must go – and if you can hold your land you can live – no one can rob you of land -“

And the old man let his scanty tears dry upon his cheeks and they made salty stains there. And he stooped and took up a handful of the soil and he held it and he muttered, “If you sell the land, it is the end.”

And his two sons held him, one on either side, each holding his arm, and he held tight in his hand the warm, loose earth. And they soothed him and they said over and over again, the elder son and the second son, “Rest assured, our father, rest assured. The land is not to be sold.”

But over the old man’s head they looked at each other and smiled.

There are a further 2 books in this series, but honestly, the final two aren’t a patch on The Good Earth.

Retirement Reading Quest – Reading my way to ‘free’ council rates.

I’m on a quest to borrow and read enough books to, in effect, cancel out the cost of my council rates per year.

It’s outlined in this post.

Years 8,9 and 10: 2016/17/18 – $5,400

I may as well continue back-tracking. I moved here in 2016, so I’ll chip away at all the rates I paid up till then. I’ll need $5,400.

Running Total – $2,125.

Year 7: I’m already a year ahead on my rates, so I’m taking a reader’s suggestion and I’m going to go back and start covering the rates from the year before I started. I may as well.

Year 7: Total needed: 2019/2020…$1,800

Finished! 12/12/2025

Year 6 (2025/2026) $2,590 AREADY COVERED!!!!!!

10/08/2015 – I won’t have another rates notice until August 2026, so I have time to kill. Let’s knock over a previous year’s rates, just for fun.

Year 5 (2024/2025) $2,339 and dog rego ($63) = $2,435.

Finished it before I even had the new rates notice ready.

Year 4 (2023/2024) $2,413.

Success! Not sure exactly when I passed the total, because I was waiting on the dog registrations to come through. But yes – I blitzed it.

Year 3: (2022/2023) $2,350

12/01/2023 FINISHED! Not working gives me heaps more reading time – I recommend it!