I’m not a magazine reader, so it came as news to me when someone on Twitter said that Dave from Strong Money Australia gave a shout out to a few Aussie FIRE bloggers (including me – thanks Dave!) in a Money Magazine story about the FIRE movement in Australia.

Of course, I was anxious to read it, so I downloaded the Libby app and borrowed Money magazine from the library. (That’s another $9 off my “Earn my rates back” reading quest. ) I’d recommend reading the article for yourself, but in a nutshell, they interviewed 7 people who have either finished the FIRE path or are on their way along it. All but one were younger than me and all had different ways of navigating the path towards total financial freedom.

It made me wonder what I would have said, had I been interviewed. I’ve been a single mother for well over 20 years and have brought up my 4 boys on my own, all while working as a secondary teacher. I still have two of them at home with me, while the oldest and the youngest have flown the nest.

I stumbled across the FIRE movement around 8 or 9 years ago by reading a blog called ‘Go Curry Cracker’. I remember asking him in the comments what this ‘FIRE’ acronym stood for. I was 49, I had just paid off the house and was worried about how I could ever possibly afford to retire.

Imagine my relief when I read the famous post by Mr Money Mustache about The Shockingly Simple Math Behind Early Retirement and I realised that by doing what I was already doing – (ie: saving and investing 50%+ of my take-home pay) I was on track to being able to retire at 67 with over a million dollar nest-egg. I could retire at pension age and not need to eke out my life on the pension.

That did it. I was hooked! I wanted to learn all I could about this FIRE stuff. I devoured blogs, books and podcasts. I hate Maths and numerals with a passion, but even someone as Maths-phobic as I am can learn, given enough repetition of the basic concepts.

Last year, at the age of 57, I retired. Ten years ahead of schedule.

I’m not your stereotypical ‘FIREy’ person, being older than a millennial, single with kids, coming from a career not really known for being lucrative and also being female. (And non-American…)

So what would I have said to the Money magazine people if they’d come knocking at my door? Here goes:

Frogdancer Jones* (* not her real name.)

Retired: at age 57.

Lives: beachside in suburban Melbourne with 2 of her 4 sons. Also with her 3 dogs who she possibly loves more than her children.

Career: Secondary teacher.

“I really believe that the secret to becoming financially independent is underpinned by three very important things,” says Frogdancer Jones as she pours a cheeky shiraz. “You have to know what you value in life so you can concentrate your time, effort and money on those things. You have to be able to see the value in delaying gratification – to be a long-term thinker, in other words. And you have to be willing to learn, so that when life offers up an opportunity, you can recognise it and – even more importantly, know what to do with it.”

The last point had a huge impact on the trajectory of Ms Jones’ financial life when, after years of struggling to bring up four boys and pay a mortgage on a teacher’s wage, she grabbed hold of an offer to develop her East Bentleigh property in a much sought-after school zone. This enabled her to release the equity in the property and move to a cheaper, but better, house further away from the CBD.

“Being able to pivot from my original plan to stay there until I was carried out in a pine box saved me having to work for an extra decade,” said Frogdancer. “I would never have had the courage to do it if I hadn’t have spent all of that time reading and listening to people who have already trodden the path to financial independence.”

So what does financial independence and early retirement mean to this early(ish) retiree?

“For me, the security of financial independence is an absolute gift. I left my husband back in 1997 with 4 boys under 5 and $60 cash. There were years of struggling to provide for my boys and pay the mortgage – it wasn’t easy to live off 18K/year of Centrelink benefits until the boys were all in school and I could go back to work. The frugal habits I learned back then have really paid off! If I have to, we can live off the smell of an oily rag. It took me a long time to lose the fear that I didn’t have ‘enough’ to retire on.

“Also, being able to retire at 57 is an even greater gift. For the first time in my life, I can be totally selfish. My kids are grown, I have no grandchildren and all I have to worry about looking after are the dogs and my garden. I can spend my days entirely as I choose – the freedom is absolutely incredible. I can highly recommend retirement!”

After starting to resurface after Christmas and New Year – so many naps! – I started to wonder what I might write that could interest people now that I’ve reached the goal post of every FIRE blog and actually retired.

There’s no point writing about what retired life actually feels like, because, to be honest, it doesn’t yet feel like I’ve retired. It’s the school holidays, my pay still keeps rolling in until the first day of term 1, so at the moment it still feels like business as usual. The 27th of January 2021 will be when it begins to hit home. The first school day of the year for teachers. My last pay packet ever…

But that’s still 3 weeks away. I started drafting this post yesterday but I wasn’t in the ‘zone’, but this morning I posted a comment about how I retired early(ish) on a teacher’s salary in a high cost of living city. It was in a Facebook group called Aussie FIRE discussion group, run by the guy behind Aussie Firebug. Someone replied, asking about my strategy.

I had to smile. My strategy?

Like most of us, I bumbled my way through my 20’s, 30’s and 40’s without a clue about FIRE (financial independence, retire early.) My only motivation, once I started manufacturing kids, was to provide a safe, secure life for them to grow up in. A lot of that was providing emotional security for them, but a huge part was also providing financial security. This involved things like ensuring that we always had a roof over our heads, enough food on the table and that the bills were always paid. When you leave your husband with 4 boys under 5 and $60 cash, which is otherwise known as the scariest financial decision of all, it tends to make you focus on the money stuff.

Although I didn’t stumble across the concept of FIRE until I was 50, the actions I took in the previous years accidentally set me up to be in a pretty good place to take the idea and run with it. Even though at that stage I’d just paid off my house, so my bank balance was literally $10 cash, I was primed and ready for the information.

So what enabled me to do the following: find out about FIRE when I had a paid-off house, around 100K in superannuation and $10 in the bank, and then to retire 7 years later?

A combination of the following behaviours:

The first tool, and undoubtedly the most important, was cutting my coat to fit my cloth. Otherwise known as spending less than I earned. Being frugal.

Frugality doesn’t mean being cheap – though in the early days when the boys were very young I’m sure I crossed that line a few times simply to survive. A frugal person makes sure that before they spend anything on lifestyle frills, they’ve paid the mortgage or rent, paid the bills and provided for the necessities of life. Then they tuck a little away for a rainy day in an emergency fund/investment portfolio. THEN they decide what to do with what’s left over.

The ‘decide’ in the previous sentence is very important. I feel that the main difference between a spendthrift and a frugal person is that one employs mainly short-term thinking with their everyday spending decisions, while the other employs mainly long-term thinking.

A person who deliberately decides to use frugal principles is sure to get ahead. I used to feel, especially in the early days, that every dollar I was able to keep in my wallet was a win. Those dollars I kept were able to be used to improve our quality of life on things I valued. These things are always a mix of looking to the future and enjoying the now.

Initially, those things I valued were chipping away at the mortgage, improving our car and house, paying for music lessons and sport for the kids and enabling the boys to see a little more of the world, both with family holidays and school trips. Then, as the boys grew older, getting out of debt, indulging in personal travel, (to the UK, Europe and North Korea – so far), and then investing for the future became the things I valued.

The trick with frugality is to spend only as much as you need to enjoy life now, while making damned sure you’re putting away money into appreciating assets so that you’ll be sure to enjoy life later – and not be a financial burden to your kids.

It’s a balance – I found that if Present Frogdancer put too much towards Future Frogdancer, it made me unhappy and discontented. But if I enjoyed a few simple pleasures in the here and now while continuing to look after Future Frogdancer, life became a joy.

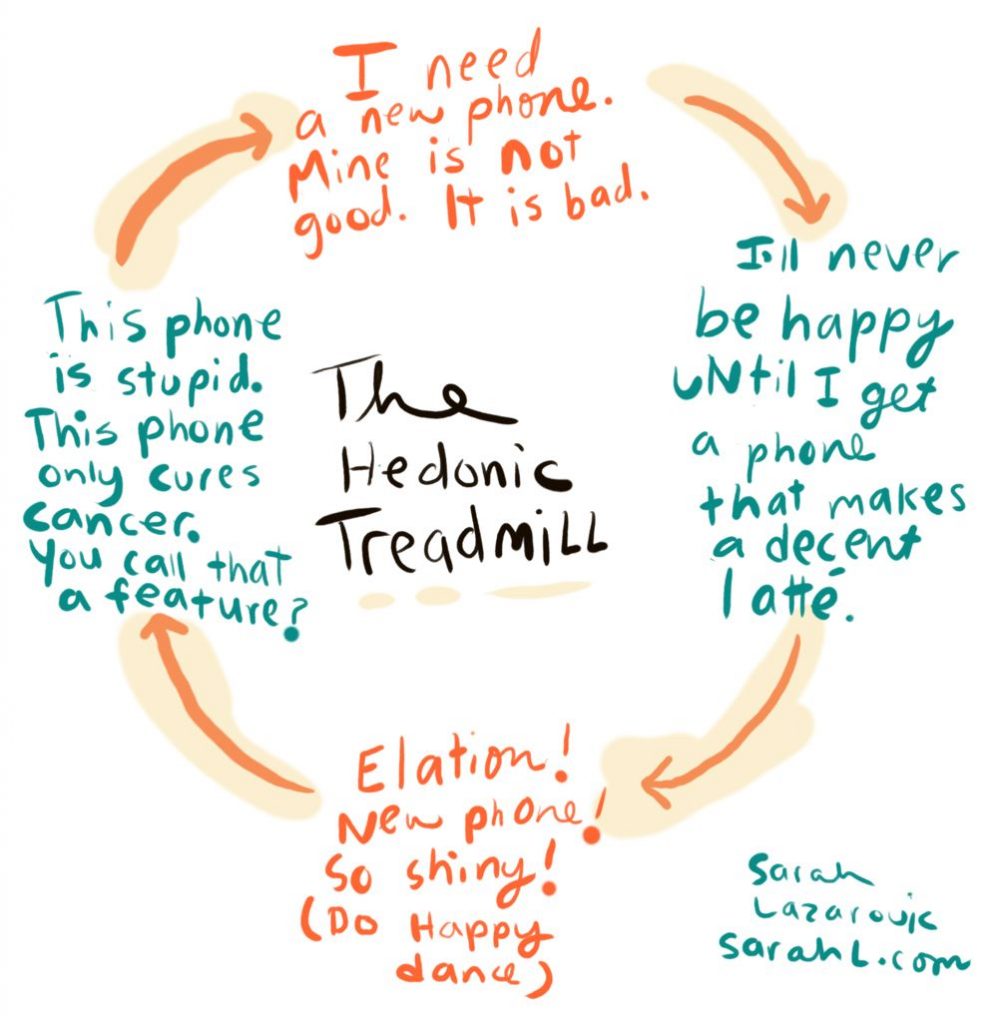

The second tool, which is closely linked to the first tool of frugality, is to recognise when hedonic adaptation, otherwise known as lifestyle creep, is threatening to happen. Then to make a conscious decision as to when, and how much, you let it affect you.

I first became aware of the term ‘hedonic adaptation’ during a Choose FI podcast when they were interviewing Barney Whiter, otherwise known as The Escape Artist. Basically, it’s when your spending increases as your income increases – at first you feel happy but then as time goes on you revert back to the happiness level you were before.

You know how it goes. You get a pay rise. You feel rich! You start getting takeout more often or going to restaurants more often, “because I can afford it.” You might upgrade the car, in order to drive something more befitting a person of your status. Clothes? Sure, upgrade the wardrobe! Get fancy furniture, buy some ski gear, buy a boat… you get the picture.

But over time, that new car doesn’t feel special anymore, it’s just your humdrum car. The boat isn’t a thrill anymore… in fact, it seems so dull and ordinary that you start to feel that you need a new one. The restaurant trips aren’t a treat anymore… they’re just a regular part of your Friday night routine. Humans tend to become used to new things over time and then crave what we perceive to be bigger and better things.

Your big pay rise doesn’t make you feel rich anymore. It’s a struggle to survive on such a small pay-packet. “No one can get ahead these days, it’s hard for the little man to survive.” You feel exactly the way you did before about your life, despite the new toys that initially brought you happiness. That’s the hedonic treadmill at work.

We live in a consumer-driven society. The trick is to only let your lifestyle increase by spending more on the things YOU value. Disregard what other people think that you should be buying. After all, they’re not going to be the ones helping you to retire early(ish!)

When I knew that I had a permanent position at my school, I took out a new mortgage to upgrade my kitchen, bathroom and the heating and cooling systems. I waited until I’d paid off that mortgage before I indulged in the overseas travel for myself that I’d always dreamed of. Could I have done both at the same time?

Yep. But I wouldn’t be retired now. Paying off that mortgage to become debt-free was crucial to becoming financially independent.

Recognising the temptations of lifestyle creep and deliberately choosing to limit your exposure to it means that you can pour your surplus money into assets that can increase your net worth over time. Again, it’s balancing the wants and needs of Present You vs Future You.

The third tool is looking to increase your income. The lucky ones are people who can negotiate pay rises in their day jobs. As a teacher in the government system, my pay was dependent on how many years I taught, so I looked elsewhere for ways to increase my income. When I became a thermomix consultant and team leader, I was able to deploy the extra money I made into paying off my house earlier and then paying cash for my decadent trip to the UK and Europe.

In other words, I used the extra money from my ‘side hustle’ to pay off an appreciating asset, (my home), and then used the excess funds to pay for a frivolous treat, (my trip), while all the while in the background the teaching job continued to pay for day to day expenses and investments for the future.

I did this for around 4 years. I worked my arse off between the two jobs and I was B-U-S-Y! And often very tired. But doing this turbo-charged my finances and put me in the perfect position to recognise the beauty of the FIRE concept when I discovered it.

The fourth tool is to be willing to learn.

A bit of background here: all my life I’ve avoided numerals and Maths. At school, I was in the top stream for English and at the same time, I was put into the veggie maths classes. When I see a page full of numbers my brain literally freezes and I can’t begin to work things out. I’m genuinely scared of them.

This is fine for an English teacher, but it’s not so great when it comes to learning things about the investing world.

My point is that, for me, it was HARD to start learning about how to invest. I’m sure it has taken me three times as long to understand about half what any normal person would learn in a given amount of time.

I was talking about this a year ago wth another English teacher who was asking for help with her finances. She said, “I wish it was as easy for me as it is for you, Frogdancer. I know nothing about this stuff.”

“It’s not easy for me at all!” I said. “My brain is like a rock and the information is like drips of water falling onto it. Over time, the drips make an impression, but it takes me longer than most to get it into my head.”

The tipping point for me was 3 weeks after I’d paid off my house. I’d spent three weeks buying ALL the yarn in every colour, brand new sandals, new clothes and I was happy. Then it dawned on me that you can’t eat your house. In other words, what was I going to do about retirement?

The thought of being in poverty scares me. I’ve been there, as anyone who’s read my ‘About’ page or heard my retirement speech would know. It was hard enough being young and being dirt poor – how much scarier would it be to be old and poor? I knew that the spending party was over. I had to start finding out what to do to put myself into a decent position by retirement age. In Australia, that’s 67 years old.

That gave me 17 years.

As luck would have it, the Barefoot Investor had just started an investment club, which has since closed. The first thing he put out was a ‘Rescue Your Retirement’ feature. After I read it, I literally cried tears of relief. My position wasn’t hopeless. There were ways to build a comfortable retirement for Future Frogdancer.

After that, I started reading. Books, blogs… I went down the rabbit hole. The relief I felt when I saw Mr Money Mustache’s post ‘The Shockingly Simple Math to Early Retirement’ and saw on his chart that if I saved 50% of my income I could retire in 17 years… omg. I was doing more than that already!

I just had to stay the course and I was probably going to be fine. I was on track to retire at 67 with a more than comfortable income. Phew! I could have stopped there.

But I kept on reading. The idea of having the freedom to do what I want in each and every day, unfettered by timetables, commutes and the demands of kids was beginning to intoxicate me.

I learned about different types of investments. Individual shares, LICs, ETFs, superannuation options, domestic and foreign geoarbitrage, property… you name it; I was reading about it. Like all learning, it started to open my mind to the possibilities…

Tool number 5, arguably as important as tool number 1:

ACT ON WHAT YOU’VE LEARNED, and be prepared to pivot if better information comes your way.

This sounds easy but in reality it’s really hard. No one likes the idea of losing money and making mistakes. But there’s a huge opportunity cost to sitting comfortably on your backside, deluding yourself into believing that because you’re reading about all this stuff, you’re ahead of over half the population.

You’re only ahead of the pack if you actually decide to DO SOMETHING with the information you’ve learned.

My first step was to move superannuation funds, first to the one that the Barefoot Investor recommends, but then when my friend The Mayor showed me that the default super fund in the same company actually gave far better returns, I swapped again. I pivoted slightly when better information came my way.

I began putting my savings into shares, index funds and LICs. Over time, it became my ‘shopping’ pastime. Some people shop for clothes, shoes and lattes; I shopped for shares. I looked don it as buying little scraps of my future freedom.

The brilliant thing about learning is that it opens the mind to opportunities that you might otherwise overlook. I learned about the concepts of geoarbitrage and property development, without ever thinking that I’d put them to use. Little did I know… if doing the thermomix side hustle turbo-charged my finances, utilising geoarbitrage and property development sent my finances screaming into outer space!

I wrote in detail about how I tweaked the geoarbitrage concept HERE. In the TL:DR version, I drew up plans to put 2 luxury townhouses on my house block in a desirable school district in Melbourne and moved 16 kms away to a far cheaper – but better- house 5 minutes away from the beach. By doing this, I freed up a TON of equity that was stored in that little house and shaved ten years from my working life.

This would never have happened if I’d been too scared to take the calculated risk and Just Do It.

When I think back to that 34 year old I wrote about in my ‘About’ page, sitting by the heater listening to the mice eating the bait and then I compare her situation to the one I’m living in now, the difference is enormous. I’m living the life that Past Frogdancer would never have even dreamed was possible.

It’d be too simplistic to say that the geoarbitrage decision was the one thing that brought all this to pass. It was certainly important, but I would never have been in a position to do it if not for the thousands of tiny little decisions I made along the way.

Frugality, living below my means no matter what, avoiding lifestyle creep, working to increase my income, learning about how to reach financial independence and then putting those concepts into action in ways that suited me and my family – all came together to bring me to this position.

I’m retired at 57. I can do whatever I want, whenever I want. I find that a very precious and beautiful idea and I’m looking forward to seeing how my life will unfold.

These tools aren’t the only dishes on the financial independence smorgasbord table. There are many more options and strategies available.

These are simply the ones that I used to get to where I am now. At first they were used for financial survival – then as time went on it morphed into working for financial freedom.

I hope that someone can take all of this and tweak a tool or two to use on their way to gaining their own financial freedom. The more, the merrier!

As of today, I have 108 days to go until I finish work for good.

Yes, I’m retiring.

My friend Scott suggested that I look at working days left, to make it seem even more delicious. Just counted it up. 47 working days to go.

On December 18 2020, Frogdancer Jones will be walking out of the classroom forever to go and live her best life. I’ll be 57 years old, exactly 10 years younger than the ‘traditional’ retirement age of 67 in Australia.

omg. I’ve bought back 10 years of my life.

I’m awash with excitement, anticipation and the tiniest dollop of trepidation. Its a big step, after all.

As you’re reeling back in shock, I hear you ask, “But how can this BE?”

Settle in. Here’s how it all happened:

In August an email went out to all of the staff, asking for our plans for next year. Did we intend to stay at the school, which subjects and year levels would we prefer to teach, would we be intending to take any time off etc. Without really thinking about it, I replied that I’d be working for another year at 3 days/week, just like this year.

In other words, force of habit. Inertia.

A week later, I mentioned to a friend, (let’s just call him ‘the Mayor’), that I’d signed on for another year. It was a conversation over Facebook. His reply?

“Another year. I’m a little surprised. I’ve noted your Covid-related comments and we certainly won’t have dealt with this by next year.”

Now the Mayor is the total opposite to me when it comes to a relationship with Maths. He loves analysing spreadsheets and company financials and everything like that. After my geoarbitrage deal finalised and I had the money from my house sale in my hands, he devised a spreadsheet projecting how my current investments could perform. I was so appreciative – it was a huge favour for him to do for me. So he knows my financial situation.

At the time that he drew up the spreadsheet, he said to me, “You know, you could retire now if you wanted.”

“NO WAY!!” I said. “I just don’t feel safe. “

He chuckled. “You can; you just don’t realise it yet.”

In the intervening years, I worked at making The Best House in Melbourne even BETTER – for Future Frogdancer Jones in retirement. I liked the idea of getting all of the expensive jobs over with while I still had a wage coming in. My post called ‘Why owning a home trumps renting‘ lists all the things I’ve put into this place, plus a few more that I’m thinking of.

After the Mayor’s remark about my Covid-related comments, I started thinking. Was it possible that I could actually retire?

I brought out the old spreadsheets and looked at them, comparing the projected figures with the real ones. I brought up my annual expenses chart, subtracting the costs of all the projects around the house that I’d been doing. I looked at how much I was spending to feed, house, clothe and shelter myself and the two boys I have still living with me.

That figure came in at just over 30K/year. Those meagre years have left their mark – I don’t waste any money on anything that I don’t value. My pleasures are either hellishly expensive (*cough cough Travel*) or are as close to being free that it doesn’t matter.

Hmmmm.

I contacted the Mayor again. Long story short, he’s preparing a document for me to take to a financial planner outlining everything to do with my finances, future plans and goals – all of that stuff.

Turns out I’m going to be fine.

But the clock was ticking at school. Kids were making their subject selections for next year and staffing decisions were being made. I didn’t want to jerk the admin around – getting my job at that school was the single biggest reason that I was able to dig the boys and I out of poverty. I owe the school a lot.

So, once I sat with the decision to leave for a few days and I still felt comfortable with it, I rang my boss.

“OH NO!!” was her reaction. But when we talked about the hows and whys of why I was leaving, there was nothing much else for her to say. She’s not stupid – she knew I’d made my mind up.

So why am I leaving? It’s not simply fear of getting Covid.

F U money.

FU money is a big part of it. After surviving the years at home with pre-school boys when we had hardly two cents to rub together, I’ve been hard at work ever since to do my best to ensure that we were never in that position again.

I’ve reached the position where I feel I have enough.

Enough.

I still love being in the classroom. The kids I teach are lovely and they’re so funny! It’s a rare day when I haven’t had a good laugh in class. I like the idea of going out while I’m still having fun – it’s much better than being ‘that teacher’ – the one who’s hanging on grimly to the job because s/he can’t afford to leave.

What’s getting me down is the insidious increase of admin. As one colleague said to me recently, “Honestly Frogdancer, it feels more and more that we’re becoming data collectors instead of educators.” We’re expected to measure kids’ performances all the time, with results put on tables and studies and projections – maybe the Maths/Science people like it but for me ? For me it’s sucking the soul and the fun from the job.

If I still had a mortgage to pay or debts to get rid of, I’d be staying. If I didn’t have enough to support myself on in retirement, I’d be staying. As I said, I don’t hate everything about the job. Most days are very pleasant days.

But there’s enough on the dark side to make me feel that now is the time for me to leave.

Fortunate Frogdancer strikes again! Going part-time this year, then having to spend months at home on lockdown has shown me that I have plenty of interests to fill my days. As long as the world contains books, the internet, Netflix and the dogs, there’ll never be an excuse to be bored. Spring has begun and soon I’ll be out planting seeds and designing my front yard. Yesterday I ordered $400 worth of fruit trees to plant there. There’ll be fruit to pick, cook and eat for decades to come.

I can’t see overseas travel being a thing for the next couple of years at least, but that won’t stop me planning for my trips back to the UK and Europe when things settle down. After all, I haven’t been to Windsor Castle to see Henry VIII’s tomb yet! Of course, there’ll be domestic travel as our internal borders open back up, so I’ll be well-placed to take advantage of that. (And I won’t have to wait for the school holidays when prices go up and everything is crowded!!)

Yes, it’s a big change. In one way I’ve moved quickly but in another way – I’ve been writing about retirement and financial independence for as long as this blog has been around, and I’ve been thinking and planning for it well before then! This decision has been years in the making.

I’m looking forward to what the next stage in my life will bring.

While I’m stuck here at work, putting in my last day before the winter holidays, please duck across and have a read of this series. There’s some very interesting and determined people there, who all prove that you can still retire early, even if you don’t discover FIRE until your 40’s or 50’s.

On Monday the school had people from VicSuper come out to talk with people about their retirement plans. VicSuper is the default retirement company for teachers, so the vast majority of staff are with them. I don’t have my superannuation with them anymore, but I booked a half-hour slot during my lunch hour to have a chat with someone anyway. I thought that they wouldn’t be able to talk in detail, but I could at least have someone more mathematically gifted than myself to have a look at what I’ve set up and tell me if I’m on the right track or not.

Let’s call her ‘Ms VS’. It has a certain ring to it.

For the non-Aussies: Superannuation is the name for our retirement funds. Every employer is required to pay in 9.5% of every employee’s wage into a super fund of the employee’s choice. It guarantees that by the time people reach retirement, they’ll have at least some money behind them, instead of solely relying on the Age Pension.

When we first starting talking, I said to her that although I’ve been working full-time, I’m dropping back to part-time next year as a sort of glide-path towards retirement. I said that retirement might be 3 years off (when I can access my super) or it could be as soon as 1 year off, if I find that I’m still hankering towards total freedom over my days even with the reduced hours.

Apparently, from what Ms VS said later, this is pretty standard. She said that she normally doesn’t have people book a time with her unless they’re very close to retirement, when they suddenly become aware that they’ll have to rely on what they’ve put away in their super. She clicked her pen, leaned forward and asked me if I knew what I have in my investments.

Did I know what I have in my investments?!? Little did she know that she was talking to Frogdancer Jones. I’ve been reading blogs about net worth, share portfolios, savings accounts, superannuation and the like for YEARS. Hell, with all the US blogs I’ve read, I know more about American retirement accounts than you could shake a stick at!

I was primed, ready and prepared.

I had period 1 off that day so I had time to make a full list for her. Well, to be honest, I just took all my numbers from the ‘Net Worth Table’ I have in the cloud, which I update at the end of every month. Took me less than 5 minutes. I flipped open my notebook at the correct page and passed it across.

I don’t think Ms VS meets a lot of FIRE-y people in her line of work.

She was pretty surprised, not so much at my figures, though she said they were unusual, but by how I’d thought about the share market ups and downs and where I’d pull money from when the market tanks. She didn’t need to explain how the share market ebbs and flows; how risk can affect people in different ways depending on how close they are to retirement; how, if I retired earlier than 59, how I’d have to find the money to fund my lifestyle and what a safe withdrawal rate was, etc, etc.

Thank you, blogs and books in the FIRE movement! I looked like I had a financial brain!!

The talk about my actual figures only took up about half the time, so we moved on to talk about other things, which is why I wanted to write this. Some of what she said was scary, particularly for women.

I guess when we’re interested in FI and we read all the blogs and books and start to absorb the knowledge, we assume that most people are more financially literate than they really are. According to Ms Vs, this is far from the truth.

She said that when I mentioned that I was looking to pull the pin in the next year or two, she thought I’d be like most of the people who come to see her. They give no thought to their retirement, assuming that the compulsory 9.5% of our wages that our employers are legally required to put into Super is enough. Then, a year or two out from retirement, they decide to look at their figures, they have a heart attack at what they see and they come running to see what they can do about it.

I guess that’s not so much of a surprise – we hear this a lot about huge swathes of the population not getting ready for retirement in time. At the risk of sounding like a Nelly Know-it-all though: I just don’t understand that mentality. When I was in my 30’s and 40’s I deliberately ignored putting extra money into my retirement account because I made a conscious choice to pay off my house first. Security for the boys and I was my paramount objective. But 3 weeks after I’d made that last mortgage repayment, I was stressing over what I had to do to get my Superannuation account looking more lively. Maybe that’s the blessing/curse of being a long-term thinker??

“I see a lot of women in their 50’s and 60’s who come in after a divorce,” Ms VS said. “They’ve only got around 70K in their Super and they still have a mortgage. They’ve never dealt with finances in their lives before and it’s a scary time for them.”

I smiled. “I went through the divorce thing twenty-two years ago,” I said.

“You’ve had time to recover,” Ms VS said. “It’s really good to see a woman as well-prepared as you. Though I suppose you’ve had to be organised, being on your own.”

“I wasn’t on my own!” I said. “I also had 4 kids under 5 with me.”

Miss Scout – anyone who’s owned Dachshunds, like Ms VS and I, are part of a special club. 🙂

We talked a bit about where the boys and I started from, veered off into talking about dachshunds, (because why wouldn’t we?) then back onto finances.

“Have you ever taken what you’d consider being a financial risk to get into the position you’re now in?” she asked.

“OMG, yes,” I said. “Years ago, back when the boys were still in school, I decided to take a 15K pay cut from teaching by dropping a day and using that time to run a group of Thermomix consultants as a team leader. 15K was a lot of money to me back then… well, it still is!… but I was assured that if I worked hard I could pull in 30K. Turned out to be true, so I kept doing that for 3 or 4 years.

“Then, when I decided to go into partnership with a developer and draw up plans to put a couple of massive townhouses on my property, I took on a 750K bridging loan when I bought The Best House In Melbourne and still owned the original place. The interest payments took up over 70% of my take-home pay. I thought it’d be for 6 months or so but the council took so long to approve things that it was 18 months before I was able to sell the property with approved plans and pay off my new place. I was terrified the property bubble would burst, but it turned out that I sold at the peak of the market so, in the end, it worked out. It was a calculated risk – but it paid off.”

We talked about whether I’d seen a financial planner. I said I hadn’t and she said, “You’ve managed very well so far, so why would you hand it all over to someone else and pay them a fee to look after it for you? “

I said that before I leave work, I want to see someone to stress-test my plans in case there was something I’ve missed, and she thought that was a good idea.

As the bell for the end of lunchtime rang and I got up to go, she said, “It’s rare that I see someone who’s all over it like you are – and if I do, they’re usually Maths teachers.”

I’m glad that I was able to fly the flag for the Drama and English teachers for a change!

Late last year I wrote a post on how I sold my house, with fully-approved plans to build 2 massive townhouses on it, to a developer. I was going to do the build myself, but when I was offered a crazy sum of money to sell the house ‘as is’, I decided that a bird in the hand was worth two in the bush, so I sold it.

Last November it was passed in at auction. In the time between me selling and them building, the wildly expensive property market in Melbourne had begun to soften. They had a reserve of 1.6M for the right-hand townhouse, but at the auction they didn’t even get one bid. Standing with my old neighbours watching this unfold, I felt bad for the developers. They’ve done a beautiful job on the build. I was also incredibly thankful that I’d made the decision to sell when I did.

Since then they’ve reduced the price twice and last Saturday it went up for auction again. I was planning to drive down to see it, hoping that this time the developers would get lucky. It’s all too easy to put myself in the situation and imagine how I’d be feeling.

I was paying bridging finance for The Best House in Melbourne at 72% of my take-home pay for 8 months, then when I dropped my gig as a thermomix consultant and went back to full-time teaching it was “only” 55% for a further 8 months or so. Imagine if I was still paying that today? I would be beside myself with worry if it didn’t sell.

The reserve price at the last auction was 1.6M. On the actual ‘For Sale’ on the website, it now suggests a range of between 1.4M – 1.480M. I was interested to see where the sellers’ heads were really at. The lowest suggested price on a real estate board is rarely what the sellers will accept!

But, just as I was planning to get ready to leave, I thought I’d check the website to make sure I had the auction time correct. This is what I saw:

There was no sticker on the board at the front of the property yesterday morning, but when I rang Tom27 he said that he drove past in the late afternoon and saw them putting the ‘Sold’ sticker on it then. You’d think he’d tell his mother straight away, but I guess not…

I sent a text to the real estate agent, asking what they got for it…

… then I waited. Saturdays are a busy time for real estate agents.

The suspense was killing me…

… and then he rang.

The townhouse went for 1.45Million, with the buyer paying an extra 47K for modifications to be done to the house by the builder. Imagine having the money to pay an EXTRA 47K to pay for ‘improvements’ after you just spent just under one and a half million dollars…?

I’m so glad for the builder that he finally managed to sell this property, but the scary thing is that he had a reserve amount of 1.6M back in November and had to drop 155K off his projected profit to be free of it. That’s a substantial amount of money.

Still, no doubt he still made a profit. I’m also VERY glad I took the money and ran when I did. Part of financial success is hard work, attention to detail, making a plan and sticking to it for a long time. And part of it is timing.

Clearly, I’ve benefitted from both. May we all be as fortunate!

I’m sure that I’m not alone in coming relatively late to this whole FIRE thing. Surely not everyone who latches onto this idea of financial freedom is a bright-eyed twenty or thirty-something who has all the time in the world to get their financial act together and then spend untold decades doing exactly whatever they want to do.

Some of us must surely be like me. I spent my twenties beginning my career, breeding and showing dogs as a hobby, getting married and starting a family. You know… the usual. My thirties were spent raising my boys, divorcing my husband and then re-establishing myself back into my career field. I was paying my bills, supporting my family and doing all the right things that were expected of me. I focused on becoming debt-free and paying off my mortgage, which I did just before I turned 50. I knew dimly that it wasn’t the best decision in a mathematical sense, but security was extremely important to me, so it was the right decision for me. I paid off the house.

But what then? I looked ahead and saw that unless I started getting serious about investing, I’d be doomed to confiscating mobile phones, trotting around on yard duty and marking essays until I was 70. I love teaching, but I don’t think it’d be much fun doing it in a zimmer frame. But I knew absolutely nothing about investing, aside from vague references to “blue chip shares” and seeing the 10 seconds worth of financial stock market stuff on the news every night.

I was scared. Literally scared.

I’m sure I can’t be the only person who has felt this.

I joined an investment group with the Barefoot Investor, which back then was wonderful… but has since devolved into a product that isn’t as good as it once was. But at the time it was great. I started a small share portfolio, made some very savvy friends and felt a little better. I was doing something, and action always feels better than inaction.

But then I started wondering. How much is enough? How do you know when you have enough to retire? I come from fairly long-lived stock. Two of my grandparents lived till their mid-90’s. Grandma was left in a comfortable financial situation by her husband, but my Grandad on the other side of the family ran out of money in his late 80’s and had to rely on my parents to prop him up when he needed more than the pension. He retired when he was 59 and I’m positive that he would’ve thought that he’d be fine. Looking at the two different scenarios, I know which one I’d rather be living when Old Lady Frogdancer hits 110 and is planning her next trip overseas…

But given all this, how do you know what amount of money to aim for?

Soon after joining the Barefoot Blueprint, I stumbled across the world of personal finance blogs. I’ve been blogging since 2008, but I was primarily in the crafts and permaculture world. The personal finance area was a revelation of education and paradigm-widening information. The very first blog I found was Go Curry Cracker – in fact, I asked him in a comment what FIRE meant. Talk about coming late to the party! One of the first posts I read was about this thing called the 4% Rule. I was intrigued but didn’t fully understand, as Jeremy went into a lot of advanced graphs and Maths, which wasn’t great for someone like me who didn’t have their head around the concept and was scared of Maths. (Still am.)

Then shortly afterwards, I found the blog post that so many people reference and point to as the one that explains it all. Mr Money Mustache’s post about the shockingly simple Maths about retirement. (I’ve included a link at the end of this post.)

It blew my mind.

The 4% Rule is based on a massive mathematical study that some uni guys did in Trinity University, where they studied how many portfolios would last over a 30-year span, based on differing rates of spending over that time. They studied what would happen if people started their retirements in every year, starting from 1926 in rolling 30 year periods. They demonstrated that in a portfolio of 50% shares and 50% bonds, (which is WAY conservative), you’d end up with money still in the kitty in 96% of cases if you kept your spending to 4% of your portfolio. Many times, you would have ended up with MORE money in your portfolio than when you started. Not bad odds…

I’ve included the links with all the Maths at the bottom of the post. No way am I going to try and explain all of that when others have already done it so clearly. Plus, you know… Maths. *shudder*

But the crux of the matter is that if you take your anticipated annual spend and multiply it by 25, you get the number that you need to stash into your portfolio to be able to support yourself in retirement. I have no idea how or why it works; I think it’s magic or something. But this is the way to find your number.

Now THAT gives you something to aim for. I dare you… think of a figure you think you’d need to live on and times it by 25. That’s how much you need to have amassed in savings/investments before you should think of retiring if you want to be a self-funded retiree and not totally rely on the old-age pension. As long as I have a calculator handy, even I can do that. I can tell you, I was dancing the fandango when I realised that I finally had something concrete to aim for.

The amount of money will be large. For example, if you think you could live comfortably on 40K/year, you need a cool million. 50K? that’d be 1.25 million. 60K? 1.5 million. At first sight that’s intimidating, especially if, like me, you’re starting a little later than some.

The beauty of it is that we have a lot of control over most of it.

Here in Australia we have a pretty good system with regards to superannuation. Every employer has to pay 9.5% of your wage into a super account that YOU can choose. Most people passively go into the one that the employer selects for them, but with a bit of homework on some comparison sites, you can work out pretty quickly if this option is the best one for you. If you decide you’d prefer to have your money work harder for you in a different fund, it’s extremely easy to change.

So you already have nearly 10% of your wage going into super. You may choose to let this bubble along if you’re young and have plenty of time on your side while making other investments along the way. If, however, you’re like me on the shady side of 50, super is an excellent way to accelerate your savings for retirement. The tax advantages are huge.

I’ve had a couple of conversations lately with people who still don’t salary sacrifice. It’s scary to think of how many people there are who don’t take advantage of this excellent way to get more bang for your buck while saving for Old Lady/Man……..(insert your own name here) …’s quality of life. If you choose to salary sacrifice, every dollar of your wage that gets taken out and put into super is taken out FIRST. It’s taxed at only 15%… then the rest of your wage is then taxed at your normal amount. This means that even though you may choose to salary sacrifice $600/pay like I do, you get more money in your pay than you’d initially think. My wage didn’t drop by $600. It only dropped by $450 or so, which means that I have an ‘extra’ $150 to play with. Again, it’s some magical incomprehensible Maths thing. But without a word of a lie, every single person I’ve persuaded to start salary sacrificing comes up to me after their first payroll deduction and says something like, “I can’t believe how much money I’ve still got!” It’s true – you steel yourself for your pay to drop by the amount you’ve nominated, so it feels like you’ve received a pay rise when you get more back than you were expecting. You can put in up to 25K a year, including what your employer puts in. It’s brilliant.

We also have a HUGE amount of control over our annual expenses. After all, this is the figure that will determine the ‘times 25’ of the 4% Rule. If you have a burn to retire earlier than age 67, then if you reduce the amount you need to live on, your magic retirement goal number will be less. This is why I call myself a value-ist. I’ll spend big bucks if I have to on the things I think bring joy and value to my life, (hello$2,000 miniature wire-haired dachshund!), but I’ll either drastically reduce or eliminate the things I feel that don’t.

For example, everyone talks about the latte factor – how if you stop buying that $3.50 cup of coffee every day when you go to work you’ll save $840/year. We’ve all heard it. My sister Kate and I have vastly different attitudes to buying a daily coffee. To be frank, I think it’s a waste of money. My school actually supplies plunger coffee, tea and instant coffee for free. My attitude is, ‘Thanks very much!’ Do you know how many people in my staffroom walk up to 711 to buy a coffee every morning? Then during the day, someone will say, “I’m just popping up to AJ’s for a coffee. Anyone want one?” and the hands go up. I don’t get it. They have the common room to sit and socialise, just like in a café, and they can get their coffee for free. My sister, on the other hand, derives immense joy from her daily coffee. She loves trying out different places, the different tastes of coffee beans, the social aspect of a busy café… for her it’s an expense she feels adds a huge amount of enjoyment to her life. You’d have to prise that coffee out of her cold, dead hands before she’d give it up, so she continues to spend money on this, whereas I have almost totally eliminated it from my life.

When you get the bug for organising yourself towards retirement, one of the most useful things you can do is to track your spending. Over time, you can see where the necessary spending is and, most importantly, where the wasteful spending comes in. Then it’s a simple matter to plug the holes and bring your annual expenses down. When we become aware of those little day-to-day purchases that are so small that we disregard them at the time we make them but which can add up over time to be almost frightening… this is definitely an empowering thing to do in life. Once you’re aware, you have the choice to continue along the same path or to change. If you’re never aware; you can never have the choice.

I guess what I’m saying is that conscious frugality in the areas that suit your life is a cornerstone of the FIRE life. That’s why I’ve decided to include “Frugal Friday” into this blog.

Another way to accelerate your savings towards your magic number is to increase your income. I have no useful input with regard to getting promotions and pay rises from your job. I work in the public sector in the education field, where pay rises are automatic each year and promotions are limited in the school I’m in, so I have no real experience. But a side hustle? THAT I know about.

Sacrificing a little bit of tv watching time to bring in more dollars is the classic short-term pain for long-term gain thinking. I did this for years, searching for a solid money-making opportunity that would be worth my while. My last side hustle enabled me to pay off my house years earlier, then to save and pay cash for a 30K trip around the UK and Europe. Then I funnelled the cash I earned into investments. Was it worth my while? If you’d asked me that when I was swanning around Hampton Court Palace in a red velvet cloak, I would have laughed in your face. My side hustle was tiring and made my life much busier, but it enabled me to get out of debt which then freed up a large amount of money that I could direct into investments and an extravagant trip of a lifetime without sacrificing my savings towards super and shares. If you eliminate debt it enables you to turbocharge your path to your magic number.

One of the best days of my life! Thank-you, side-hustle.

A wonderful thing to keep in mind is that you have control over the magic number you aim for. Personally, I’m keeping current annual costs as low as I can, while working towards an annual figure far larger than I need to live on to survive. My magic number is designed to let Old Lady Frogdancer thrive! Therefore, my personal 4% Rule number is inflated beyond my current spending, to take into account all the travel I intend to do. This is an easy decision for me to make as I still enjoy my job and don’t mind working a few extra years to build up some more money. Someone else may be in a different position, where they hate their job and by cutting unnecessary expenses they can bring forward retirement and they can start enjoying the freedom of that lifestyle. We all have great control of our own paths – if we make conscious decisions.

I’m a big fan of the 4% Rule as it’s an easy formula to get your head around. For someone just starting to grapple with these ideas, it gives you a giant bulls-eye to aim at, which is incredibly empowering. Later, as people get closer to the time they decide to pull the pin, their investment decisions can be modified to their individual requirements. Who says you HAVE to pull out 4% every year? You may decide to go more conservative with a 3.5%, or more aggressive with a 5% rate of withdrawal. You may choose to factor in a part-pension, or to remain totally self-funded. You may want to leave a legacy to family or charity or go screaming to the finish line of life clutching your last dollar in one hand and a martini in the other. Those more detailed plans can come later, as you become more educated and you start fine-tuning your investment plans. But for broad-brushstroke planning, the 4% Rule offers as much certainty for forward planning as you’re likely to get.

***

Here are the two articles that sent me on this path. I’ve included the simpler one first, with the more detailed one following for those who want to go deeper into the concepts. The comments are well worth reading too, as people query and discuss things. They bring up points and debate them, which deepens the knowledge, which is a pretty good thing.

Mr Money Mustache’s post on “The Shockingly Simple Math Behind Early Retirement” is HERE.

Go Curry Cracker’s post on “What is Your Retirement Number – the 4% Rule” is HERE.

(This is one of my Christmas presents. My youngest son Evan21 took the photo and then blew it up – we now have a picture of the whole family. )

*** This is the post that won the first Rockstar Rumble in 2018 – the blog tournament run by Rockstar Finance.)***

When I was married, waaay back in the day, I was working as a teacher in a suburb on the outskirts of Melbourne in the west. It wasn’t where I grew up, (I’m a Bayside girl from the other side of town), but it was where my husband had his business and love makes you do crazy things like move across the other side of the city to live.

We delayed starting a family, so in the meantime I discovered dog breeding and showing. Poppy and Jeff, in the photo above, are descendants of the dogs I bred at that time.

For 6 years dog breeding was my passion. I wanted to have a place where I could build proper kennels and give them space to run. My husband was a country boy and he wanted space around him, so we started looking for a block of land. We found one on the outskirts of Bacchus Marsh. 6 acres, already fenced. I can’t remember what the asking price was, but I know that we didn’t have the money up front for a deposit.

My husband used to spend everything he made…. but that’s a topic for another blog post. The only way we could come up with the money was if I cashed in my superannuation.

At that time I was about 27, I think. I had 30K in super that was ticking along quite nicely. In those days if you wanted to withdraw your super it was really easy, so that’s what we did.

Argh!!! I can’t believe I was that stupid! I had no idea of how compound interest worked, or of the importance of letting funds deposited while you’re young in an account like super being left to slowly compound and grow while time is on your side. Nup! We wanted that block so we took the money out. A classic case of short-term thinking.

While I was sitting here I just plugged the figures into a compound interest calculator. $30,000 for 30 years at 7% interest, with no further contributions being made. That $30,000 would have been worth $243,495 to me in another 4 years. Do you think that would make a difference to the when and how of my retirement plans if that tidy sum was added to my super? Do you think I’d still be working full-time, or would I have eased back to working 3 or 4 days a week if my super had an extra quarter of a million dollars?

That block in Bacchus Marsh cost me around a quarter of a million dollars.

Do you want to know the kicker? When I got pregnant with Tom25, we decided to sell the block and an investment property we had. My husband was suddenly nervous about servicing those debts on just one wage. Property values had fallen… we ended up selling the block at Bacchus Marsh for 30K LESS than we paid for it.

Yep.

At the time I was blissfully unaware of how costly those two decisions were. But now I know that if I’d understood the power of compounding, I would never have released the funds from my super.

So I look now to my boys – those giants in the photo at the top of the page. I left the marriage when Tom25 was 5, Evan 21 was 11 months old and the other two were somewhere in between. I’ve raised them on my own and it’s up to me to teach them what I can about life, including their financial lives. If they can get their heads around compounding, they may be intelligent enough to not only avoid making the same mistake I did, but to actually turn it on its head and start actively harnessing that power.

Earlier this year I sold our property and made a profit. I’ll discuss this at some stage later on on the blog. With Christmas coming up, and with the knowledge that I’d have not only my boys but also my nieces here, I decided to be a little theatrical and give them a gift with a string attached.

I handed out these ‘certificates’ at the end of when we were handing out the presents, when I had everyone’s attention. The accompanying documents were two tables I’d printed out from a compound interest calculator site. I wanted to make it crystal-clear what I was actually giving them.

The first table shows what they’d end up with if they deposited the 1K and then never added another penny to it. I chose 40 years @7% interest (which is a conservative estimate for the interest rate. The Australian stock market averages just under 10% per annum.)

Now of course, this table is totally unrealistic unless they choose to live off Centrelink benefits and never work a day in their lives. They’ll be adding to this amount every time they work and get paid. So I added another table – this time what would happen if they only seeded this account with another $1,000 each year.

Apart from Tom25, who’s an accountant and already has his head around this compound interest stuff, their minds were BLOWN. My nieces come from a family where money isn’t a topic of conversation and so they’re not exposed to these ideas at home. I was especially pleased that Jay18, my youngest niece, quietly came up to talk with me afterward, saying that she’d be interested in finding out more.

I also gave them all a copy of ‘The Richest Man in Babylon“. It’s a slim volume and I remember reading it when I was around their age and the lessons stuck. It’s up to them if they read it or not; I won’t be following up and nagging. I figure I’ll just present the information to them and they’ll access it when it becomes relevant to them.

The funny thing is, Tom25 said to me the next morning, “One of the books Dad’s been hassling me to read is ‘The Richest Man in Babylon’!” I laughed and said, “I’m not surprised. It’s a good book.”

I guess what this story proves is that even in the holidays, you can’t stop a teacher from teaching. I’ve put the information about compound interest in front of all 6 of them and now it’s up to them how it percolates in their brains. It’ll be interesting to see how many of them, in a couple of decades or so, have taken the information and run with it.

Retirement Reading Quest – Reading my way to ‘free’ council rates.

I’m on a quest to borrow and read enough books to, in effect, cancel out the cost of my council rates per year.

It’s outlined in this post.

Years 8,9 and 10: 2016/17/18 – $5,400

I may as well continue back-tracking. I moved here in 2016, so I’ll chip away at all the rates I paid up till then. I’ll need $5,400.

Running Total – $2,125.

Year 7: I’m already a year ahead on my rates, so I’m taking a reader’s suggestion and I’m going to go back and start covering the rates from the year before I started. I may as well.

Year 7: Total needed: 2019/2020…$1,800

Finished! 12/12/2025

Year 6 (2025/2026) $2,590 AREADY COVERED!!!!!!

10/08/2015 – I won’t have another rates notice until August 2026, so I have time to kill. Let’s knock over a previous year’s rates, just for fun.

Year 5 (2024/2025) $2,339 and dog rego ($63) = $2,435.

Finished it before I even had the new rates notice ready.

Year 4 (2023/2024) $2,413.

Success! Not sure exactly when I passed the total, because I was waiting on the dog registrations to come through. But yes – I blitzed it.

Year 3: (2022/2023) $2,350

12/01/2023 FINISHED! Not working gives me heaps more reading time – I recommend it!

One of the best days of my life! Thank-you, side-hustle.

One of the best days of my life! Thank-you, side-hustle.