Yesterday I had all the kids (except Izzy) over for lunch. Ideally, I like to catch up with them in between trips, but it’s like herding cats now that they’re all adults with their own lives. Last week on the ‘Wednesday W’s’ post, I showed a photo of 4 generations of engagement rings, from my great-grandmother, grandmother, my mother and me. Yesterday Sophie was there with Tom 33, so we lined the rings up again and took another photo.

5 generations!

My great-grandmother’s ring is a crystal. It’s cracked, as I found out when I recently had it cleaned and the claws fixed. I left it as it was. She was very poor – she was a washerwoman, I believe.

The next generation was slightly better off. If you look closely, you can see that my grandmother’s ring has tiny diamond chips. Fancy.

Mum’s ring is next. It’s an actual diamond, though, “We had no money, so the ring is more setting than diamond!”

Mine is next. We used to call it “The Rock.” Personally, I wanted an emerald with two little diamonds either side (which was a ring I eventually bought for myself when I took the kids to Thailand, years after my divorce.) My fiancé was a first-gen immigrant from a desperately poor family. He was running a fruit shop. He wanted a statement ring. The Rock is certainly that.

Sophie’s ring is another diamond, but this time it’s a black diamond. She is an avid skier, and Tom33 bought a black diamond for her, as they are the most prized of the ski slopes.

In the photo above, Sophie’s ring has caught the sunlight. Here’s what it looks like normally:

What I find fascinating about these rings is that it shows the definite improvement in the fortunes of a VERY working class family. I was the first person to finish secondary school and get a uni degree in my Mum’s family. We were certainly not rubbing shoulders with the Vanderbilts and the Rothschilds! And yet, a luxury item like an engagement ring slowly became more and more valuable over time, to the extent that the last one in the line – Sophie’s – is now chosen not for actually having a diamond, but is now chosen for the TYPE of diamond.

Every time I hear that living conditions are sliding and that things have never been worse, I know that’s absolute bull5hit. Every student of history knows that life for the common person has never been better than it is today.

For example, who in their right mind would want to go back to live in medieval conditions? Nowadays, our standard of living is better than kings in that era. Every time we reach out and casually switch the heater or the aircon on, we’re winning. Putting the foot down on the accelerator, instead of riding on horseback or worse – being jolted around in a carriage with little suspension and dirt roads. Streaming practically any show we can think of, instead of waiting for a minstrel or travelling players to come and provide entertainment.

Try living in the squalor of life in the tenements in the Victorian era. All throughout history, imagine walking across the street with horseshit all over the roads, chimney sweeps as young as 4 being forced down chimneys, the Black Death killing between 30% and 60% of Europe… yikes. Obviously, the list goes on, but I have gardening to do and those garlic bulbs aren’t going to plant themselves.

This really hit home to me when I was in my early forties. I had been single for a decade or so and I was wondering if Mr Right was ever going to come along. (Strangely, men weren’t queueing up to be with a broke single mother of four boys. God knows why!) I was watering my front yard, having a quiet whinge to myself, when the thought suddenly occurred to me that I was an ungrateful idiot. I thought of the MILLIONS of women from the past who would have killed for the chance to live the life I had.

I was independent, with total control of my finances, where I lived, and how I chose to support my family. I was freely able to divorce my ex-husband AND keep custody of our kids. I wasn’t tied to someone else’s choices with money and life decisions. I was captain of our own boat.

I was educated and so I was able to support my family by teaching, instead of farm work, cleaning or lying on my back. My children were also being educated and they’d have opportunities far beyond what the ordinary women of the past could have dreamed of for their children.

We were vaccinated, could vote, and cook with the flick of a switch, instead of building up a fire every day. I was free to travel as widely as my time and finances could allow. (I had no idea what amount of crazy travel waited me though!) I had total freedom at home to do, say and be whatever I wanted.

Tell me when in the history of humankind have ordinary women ever had this much freedom and autonomy?

That very moment was when my life changed and I realised that I’m one of the luckiest people on the face of the earth. My life was immeasurably better than any generation of women before me.

The engagement rings are a tiny example of this. Over time, society is slowly getting better and better. Hell, in my travels in even the poorest of countries, every single vendor of every single tiny roadside shop selling fruit, veggies, and clothing all have a mobile phone. It’s universal… everyone scrolling through their mobiles while they wait for customers.

Are things perfect now?

Haha, of course not. There’s still so far we have to go in so many areas. Please don’t troll me in the comments by saying, “Oh yeah??? Well what about blah blah blah.” We’re living in 2025, not in Utopia. But looking back and comparing, things are not so bad.

Even a cursory look at history will show that slowly but surely, we’re crawling out of the mud to stand up and gaze at the stars. We’re the luckiest people to have ever lived. I’m not sure that we take the time to appreciate that enough.

Well, the shit has pretty much hit the fan, as far as independent living for my mother is concerned. This is Mum on Sunday night, putting on a brave face.

While going to bed, she went to sit down on the foot of her bed and only half made it. She fell onto the floor and dragged her left hand across the wooden floorboards. Her skin is paper thin, so she tore a very large gash along the back of her hand.

Fortunately, Georgia and I were talking in Georgia’s room, so we were right next door when we heard the thump and the cry as she hit the ground. We raced in, helped her to sit up, but when I staunched the blood and saw the wound, I said, “Mum, this is going to need stitches.”

We spent all night at Frankston Emergency, getting home at 5 AM. We all had a long nap that afternoon, including the dog!

I’ll spare you all the photo I took of the cut on her hand.

Anyway, living with Mum for two and a half weeks has brought home just how unsteady she is on her feet. She said it herself when Evan28 rang and said to her, “Oh Gran, what have you done?”

She said, “I’m always on the brink of falling and sometimes I don’t get away with it.”

After talking with my sister Kate, I rang Mum’s case manager for her care package and asked her what the next step would be.

Long story short, I talked with a woman who finds places for people in aged care places. I knew Mum would want a shared room for when Dad comes out of the rehab hospital, and we were lucky enough for a place literally 5 minutes drive from me to have a suitable room. Shared rooms are as rare as hens’ teeth.

So Kate and I had to have ‘the talk’ with Mum about going into respite care. We were very careful not to allude to permanent care, but really, that’s what she needs. We’re crossing our fingers that the penny will drop for them once they’re there, and it will become their own idea to stay there. This apparently happes quite a lot, but I’m not holding out much hope for Dad. He’s extremely attached to his possessions.

Mum and I went to look at the place yesterday and to my relief, Mum was very impressed. She is very happy to entertain the idea of moving in for a while, but she’s worried about Dad’s reaction. She’s also scared of rushing into a decision and possibly making a mistake.

My feeling is that we were incredibly lucky to find a shared room so close to me. It’s been a week and no other shared rooms in the area have turned up, so we need to grab it. We have until tomorrow to accept or decline.

When Dad and Mum were ill a year or two ago, I started educating myself on how the Aged Care system works. I had a real ‘heads up’ from a friend who has the affectionate nickname of ‘the mayor’ who has been through this learning curve when his mother went into care a few years ago. At least I understand talk of RADs and such. I hate to think of how bamboozled I’d feel if I was coming in cold.

The facility manager recommended we hire an accountant who specialises in the ins and outs of going into care, which I thought was good advice. My parents don’t have a straightforward estate. I rang their accountant and he’s getting someone for us to talk to.

Despite Mum reading all the material and being there when the manager was showing us around, she still worries about things that aren’t issues at all, and gets things wrong. I find that I’m gently correcting her, in the hopes that the correct information goes in and she’s not needlessly fretting about the incorrect stuff.

The idea is that she’ll move in next week under respite care and Dad will join her. They’ll stay while I’m in Vietnam and hopefully by then they’ll be able to make sensible decisions about their futures. (I know… I’m an optimist.)

A lot depends on how well Dad recovers from this broken hip. It’s not a pleasant stage for them to be going through.

Last week I received a text from the guy who used to share a flat with Tom31, asking if he could call me. Although Tom31 left the flat on bad terms with this guy, it’s been over a year since that all happened, Tom31 now has his own place and they have friends in common. They now have a civil relationship. Let’s call him Fergus.

I also knew that Fergus had unexpectedly lost his Mum a few days before. Fergus and his Mum were close and she also had a great relationship with my son. She did the conveyancing on his property and only charged him ‘mates rates’ and they always got along like a house on fire.

Of course, I took his call.

What followed was heart-aching.

Fergus was still reeling over his mother’s death. He called me because he really wanted to keep his Mum’s house and he wanted some unbiased advice. He has two siblings who want to sell it and split the proceeds equally.

“How much is your Mum’s place worth, roughly? Is there a mortgage on it?’ I asked.

“It’s worth around 1.2M and she paid it off,” he said.

“What assets do you own?” I asked.

“I have around $500 in the bank,” he said.

I sighed. “I’m sorry Fergus, but no bank will lend you that much money if you have nothing to offer as collateral. You’ll have to let the house go.”

He sighed as well and said that he thought so, but he wanted to hear it from someone who wasn’t out to make something from the sale.

He’d said earlier that the house was like a refuge for him – that when he’d had a rough day, he’d “get off at her station, go around there and we’d solve the world’s problems over a bucket of wine. “

I gently said, “You know how you talked about her house as being like a refuge? It wasn’t the house; it was the person. I suggest that you go around there on your own one day, walk around and quietly say your goodbyes. Then once the house is sold, you can move forward with whatever money you get from it as her legacy.”

“That’s the problem,” he said. “I don’t know what to do with it. I’ve already had people making suggestions about investments, but I feel so confused.” He added bitterly, “Her body isn’t even cold yet and people are already picking at what she left.”

Yikes. It was a few days before the funeral, so I totally got what he was saying.

What could I say? I’m not a numbers person. But then I thought: what advice would I want someone to give one of my boys if I suddenly popped my clogs? I’d want them to be given advice that was safe, conservative, and would be easy to implement when they were still grieving and not able to think clearly. Advice that would allow the dust to settle before any life-changing decisions were made.

It also had to fit in with the stage of life Fergus is in.

He’s not in a relationship. He’s not starting a family and looking to put down roots in a house that will suck up all of his money and shackle him into a mortgage for the next two decades. (This is the position one of his siblings is in – they’ll be using the money as a house deposit for their young family.)

Fergus is still studying. Once that’s done, he’ll be putting his efforts into establishing his new career. Who knows? He may decide that he wants to spend that money on buying into a law firm somewhere. He may choose to relocate to another city or country. His options are wide open. He probably needs that pool of money to be safely waiting for him.

Yes, he might make a few extra dollars if he put it into shares, but I still think that on balance, safety trumps a little profit. Besides, the way the share market has been bouncing around? A little profit isn’t exactly a certain bet in the short term.

I decided to go with the term deposit route. Luckily for him, interest rates are better on savings accounts than they have been for a long time.

My advice was to put 90% of whatever money he received from his Mum’s estate into a term deposit and to leave it there for 12 months.

“The other 10%? Spend it. Go on a big holiday, buy some clothes, furniture… whatever you want. She’d want you to enjoy it. But DON’T spend any more than that. Respect her legacy and only deploy it for something that’s going to establish your way in the world – whatever that turns out to be.”

I then added, “And for God’s sake don’t put any of it into crypto!”

He laughed ruefully. “I’ve already been burned by that,” he said.

“Hey, how lucky is it that you learned that lesson when you didn’t have a lot of money to lose?” I said. “Don’t beat yourself up over it; just be glad that you’re not going to make the same mistake with your Mum’s money.”

“I definitely won’t! he said.

“If you do what I’m saying, it gives you time to move through your grief and not risk making big decisions when you’re not thinking clearly. Then, when the dust has settled and you have a clearer idea of what you want to do, then you can make decisions that aren’t going to be based on raw emotion. Besides, speaking as a single mother myself, it’s hard to pay off a house on your own. You don’t want to waste her final legacy for you.”

‘You’re absolutely right,” he said. “That’s the last thing I want to do.”

At the end of the call he thanked me, saying that he felt at peace for the first time since all of this stuff started to come up.

“I think I’ll do what you suggest,” he said. “It sounds really sensible and it gives me time to breathe. Is it ok if I call you again when it comes closer to the time?”

Of course I said yes.

But this conversation really gave me food for thought.

We all expect to live till we’re old. My own parents are both in their 80’s, still living together at home and although they’ve slowed down, they’re still going strong. I don’t know about you, but any thoughts I’ve had of my children inheriting my estate have them all as grey-haired old men, with decades more life experience behind them than they have now.

But what if a similar thing happens to us? Fergus’s Mum was only in her late 60’s.

How would the boys make these huge financial decisions if I suddenly wasn’t here?

It’s a big responsibility to suddenly have a large sum of money given to you at any age. Not many people in their 20’s and 30’s have a rock-solid plan in their minds of what they’d do with a cash windfall of a few hundred thousand dollars. (And if any of my sons did, I’d be a bit worried that they’d decide that I was worth more to them dead than alive…)

I don’t know what the answer is. Do we write a letter “to be opened in the case of my unfortunate demise” to be read aloud, giving our advice? Do we hope that older, wiser people will take our loved ones under their wings and give them excellent advice? What if there’s no one around our kids who is good with money?

It’s a conundrum.

At the end of the day, I gave Fergus the same advice, given his situation, that I’d hope that someone else would give my kids if we were in the same situation. I can’t do any better than that. It was heartbreaking though, seeing a young man almost shell-shocked with grief and yet being forced to grapple with uncharted financial waters like this.

It made me hope that my boys will never be in a position like this. At least, not until they’re grey-haired old men! But if that doesn’t turn out to be the case, I hope that they have access to someone who will give them sound, unbiased advice to give them time to come to terms with their new reality and that they’ll be able to make unrushed, sensible decisions.

Anyway, this is the sort of stuff that I haven’t given much thought to until now. When they were small, I worried more about who would look after them if I suddenly died, rather than worry about inheritances. Once they grew up, I didn’t think about this stuff because, as I said at the start, I probably believed that I was immortal.

I’ll be doing a bit more thinking about this…

Dad joke of the day:

My wife told me to stop singing “I’m a Believer” or she’d kill me. I thought she was kidding..

It’s coming up to the end of the year and I’m feeling confident that I’m going to finish a challenge that I didn’t tell you about.

Part of my financial strategy within retirement is to have a pool/bucket of money, around 3 years of expenses, that I’ve put in a term deposit to ride out a stock market crash. I rolled over that money at the end of December last year, just before – you guessed it – there was a downturn in the stock market.

I wasn’t concerned. With the piddling interest being paid on the term deposit, it didn’t worry me that I’d have to break into it to pull out some living expenses.

But then I had 3 people separately contact me towards the end of term 1, asking if I’d consider helping the school out with some CRT work because covid was making it extremely difficult to cover classes.

I owed the school big time. Securing an ongoing teaching job nearly 20 years ago absolutely saved our financial bacon. The school has been fantastic to my boys and me; I’d had 3 vaccinations by then; I could teach in a mask; and …

… maybe I could stretch the time before I had to tap into that term deposit???? WHAT a challenge!

I totally didn’t expect that I’d be working as many days as I have. So far, as of this week’s pay, I’ve brought home just over 25K in income from this CRT gig. What with dividends, my CRT wages and my tax return, I’ve more than covered this year’s expenses.

So, in effect, I’ve succeeded in stretching that term deposit into being able to last me 4 years instead of 3. I’m pretty happy with that.

When I come back from Antarctica, it’ll be time to think about how hard I want to tap that term deposit. I’m definitely not working as many days as I have this year – by the end of term 3, I was very unhappy. I was pining for my lost freedom.

However, I’m thinking that working a day a week next year might be ok. That’s around $300 take-home that I could put toward a holiday or another son’s wedding or something. It’s also true that once Ryan27 moves out, I’ll be living on my own. Working a day a week, where I’m forced to interact with people, might stop me from becoming weird.

Or at least, stop me from becoming weirder than I already am.

As I’m typing this, I’m sitting in front of a deathly quiet Maths class. After lunch, I’ll be walking a group of year 8s to the local lawn bowls club for their sport double. It’s not a hard way to earn some money. The kids here are lovely and it’s nice to catch up with my work friends.

I’ve decided that I’ll pull the pin on work this year when I have 2 weeks to go before I go to Tullamarine and try to remember how to get on a flight. I definitely don’t want to catch covid and have to postpone this holiday again!

So, being flexible and taking on some casual teaching has worked pretty well for me, all things considered. The challenge of being able to stave off tapping the term deposit for a whole year was a stretch goal for me, but I DO like to win at a challenge!

But the emotional drain of seeing my glorious freedom ebbing away is something that I don’t want to repeat again next year. I feel that I’ve helped the school out in its hour of need, and having the freedom to heavily pick and choose how many days I work is something that I’ll be exploring next year.

I have to train myself to say ‘no’ if the chance to earn money is offered. Those many years of poverty are hard to break away from.

Only 5 more days to go before I walk out the door having finished my contract teaching job. I’ve done most of the marking – only dribs and drabs of late projects and 2 tests to give out and mark – and two more yard duties, (unless Rosie hits me with an extra one like she did on Friday), and by 2:30 PM Friday I’ll be a free woman again. Thank God for early finish times when terms end.

Let me state upfront – the job I’m finishing up is by any sane person’s definition an absolute DREAM job. The money’s great; the students are respectful and funny; the people I work with are (mostly) lovely; I don’t have to attend meetings; I can leave as soon as the bell rings; the biggest physical labour is walking up and down stairs all day (and if I want I can take the lifts), and tomorrow I get a free lunch provided because it’s Diversity Week. (Lamb Rogan Josh, if anyone’s interested.) To add icing on the cake, the admin at the new campus are on the ball and are a pleasure to work with.

So if that’s the definition of a sane person’s idea of a dream job, why am I feeling insane right now?

It’s simple. After experiencing retirement, even in the midst of lockdown after lockdown, my whole mindset has changed. Now that I’ve achieved financial independence, I’m in the position to start valuing my time more than money. This is a whole new ball game.

And yes, I used a sporting metaphor. Ugh. That’s how new and strange this is.

Unless you’re born into money, everyone has to work to financially establish themselves. It takes many years of work, sacrifices and tenacity to get to a point where you no longer have to trade your time for money. Along the way, some of us get divorced, so we have to start over and do the whole thing again.

That’s fun.

But after years of work, saving, and investing while life swirls around you, you’re then at the point where going into work becomes a choice. You can choose to keep building a career that you love, or you can quietly step back from giving most of your waking hours to a job and begin to use those hours for your own pursuits.

Now, I’m not the sharpest tool in the shed, but even I knew that this would happen once I hit my magic number and stepped back from work. But intellectually knowing it and then resisting the siren call of easy money once I dipped my toe back into working again are two very different things.

Taking this 7-week full-time contract has been invaluable.

It’s easy to say that you want to get out of work if the job you have isn’t great. I mean, why wouldn’t you want to leave a job where you’re overworked, underpaid and you’re unhappy being there? It makes perfect sense.

But this job is fantastic! Yet 3 weeks into the 7 weeks I was the most depressed I’ve been in years. Not clinically depressed of course, but by God, I was miserable. But this was an easy gig that I CHOSE to do myself. It had a definite finish date so I wasn’t locked into years of indentured servitude or anything. Yet I felt like I was dragging my feet through mud to get to perform this fantastic job each day.

Now that I’m nearing the end of the contract, I’ve realised that this was actually the perfect way to experience how financial independence has truly changed my life. It’s one thing to hate going to work if the job is blah/awful, but when the job is terrific and yet you feel you’ve boxed yourself in for no real reason, then it’s obvious that certain priorities have changed.

The final nail in the coffin of knowing that I won’t take a contract again was when I had a couple of parents contact me about their sons’ abysmal performance on their geography projects. The second I see that a parent has phoned or emailed me, my stress levels go through the roof. It’s never good news. People rarely contact teachers to tell them they’re doing a great job.

One parent was pretty standard, but the other one wanted me to “give him the third degree” about why he hadn’t handed in his project because they” have tried to speak to Joe Lunchbucket [not his real name] to find out what caused the work to be incomplete but he has not given me a straight answer, so I would like you to speak to him and find out.” They signed off the email with their phone number so I could report back to them after the interrogation.

I read the email, rolled my eyes and was like, “Oh, so you want me to do your parenting for you?”

I wasn’t happy, but I did the right thing and kept the kid after class, had a chat with him about the work, resisted the temptation to use the thumbscrews or the cat o’ 9 tails, and he promised to submit the project in the next 5 minutes. All good. I walked upstairs to my desk and opened my laptop to mark his project during lunch.

There was an email from the front desk, sent 5 minutes before the period had even ended, saying that this parent was asking me to call them back and giving me their number again. Seriously??? Give me a chance to have the chat in the first place and then walk upstairs and sit down.

Oof. Some parents.

The talk with the parent actually went better than I expected. They were worried about their son, “so different after having the girls!”, and I understand where they were coming from. However, I think it was fair to say that their anxiety was a little over the top. Joe Lunchbucket [not his real name] is a good kid who is a little lazy at the moment. Sounds like a typical year 9 boy to me.

What I didn’t appreciate was the effect it had on MY anxiety levels. Disgruntled parents can cause a lot of problems for a teacher if they decide to get nasty about something. I don’t need to be here. I don’t have to be feeling this.

I’m definitely over it.

Another little moment was when I was having dinner with a longtime friend a couple of weeks ago. He said to me, “But don’t you have enough money to live on for the rest of your life? Why are you doing this for? How much is enough?”

Hmmm. He got me there!

I’ll more than likely do the odd day of CRT teaching going forward. The job itself is great and it’ll be a nice day of catching up with friends, writing Dad jokes on the board and bantering with the kids.

But feeling miserable in the midst of the perfect job was a definite sign that my life and priorities have moved on. I’ve ticked the “money/security” item off my list of life goals.

Time to get back to living every day on MY timetable again.

Dad joke of the day:

Ok, so not really a Dad joke but it made me chuckle anyway.

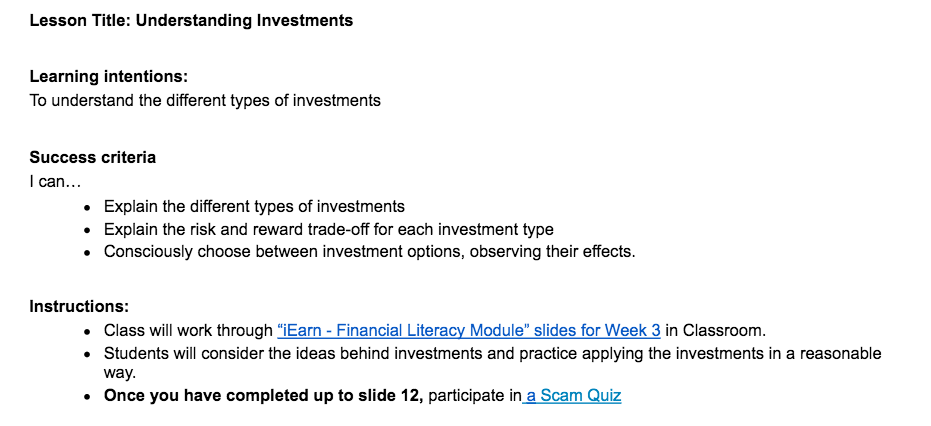

When people whine and say that “kids should be taught personal finance in schools!!! Wahhh wahhh!” you can tell them to pull their heads in.

This was the lesson plan of the first class I taught today. It’s a year 9 class that every kid takes, where they learn about our political system, how to manage money and invest, careers advice, the media and lots of other things.

As you can see by the lesson plan, kids ARE being taught real-life lessons about money and how to handle it.

The hook for the lesson was a 3 minutes news report that I played on the interactive whiteboard. It was about Afterpay and similar companies, and how people are running amock with it in the short-term and then living to regret it in the long term, as the levels of debt they rack up make it impossible to get mortgage loans from banks.

Then they went on to what the lesson plan outlined. Learning about different investments and going on to “Consider the ideas behind investments and practice applying the investments in a reasonable way.“

This is all real-life stuff. About money and how to evaluate the best way/s to use it.

Kids ARE being taught about finances. They always were.

The only reason people think that they weren’t taught how to manage money in school is because they weren’t interested in the subject when they were teenagers and so they didn’t retain the knowledge. (A bit like me and mathematics.)

We’re preparing the kids for the future! Anytime someone tries to whip up anger against teachers/schools for not doing this, they’re talking through their… um… hat.

Dad joke of the day:

What do you call a wolf who has everything all figured out?

In the FI/RE space there’s an abundance of posts about how to get to financial independence. (Quite a large percentage are written by people who haven’t yet managed to get there themselves.) There are fewer posts written about what it’s like to actually reach FI and retire. I’ve written quite a few of these sorts of posts during 2021 – the year of lockdowns and my blissfully happy first year of retirement.

But there aren’t too many posts about what it’s like to retire – then pick up work afterwards.

Surely I’m not the only person to have done this? Maybe it’s seen as a sign of shame; that somehow the financial independence hasn’t ‘worked’?

Whatever the reason that people don’t write about this much, I’m stepping up to shine a light on what it’s like to say a blissful goodbye to a career – with a kick-arse speech goodby that I’m still proud of – to then, a little more than a year later, fronting up back at the school again. As I write this I’m sitting in front of a year 9 class, tapping away here while they’re putting the finishing touches onto a political campaign they’re running. Fiddy bucks in my pocket for 48 minutes’ work, before I move onto the next class for another fiddy.

Here I am, swapping my precious time for money. This is something I didn’t think I’d ever do. Except, in the back of my mind, I had a feeling in my waters that this massive bull market probably wouldn’t keep going for another 5 years. I had a vague game plan in my mind that if the market fell before 2026, I’d probably pick up a few days of CRT, (casual relief teaching), to ease the Sequence of Returns Risk.

So, as we all know the market has taken a tumble. At the same time, schools are desperate for CRTs due to covid and the flu, along with regular things like school camps etc. I went back into the classroom as a perfect storm was hitting Australian schools.

I was lucky, in that I still loved being in the classroom when I retired, so it wasn’t as if I was dragging myself back to a job I hated. And as luck would have it, all the boring admin, report writing and diagnostic testing are things that CRTs don’t get asked to perform. Talk about a win right there!

When I began, I had a couple of weeks of a day or two of teaching, then I was suddenly plunged into a month of full-time teaching. The last two weeks have been back to the retired life with no work days, with today, Wednesday and Thursday being back at school in this last week of term 2.

So it’s been interesting to see how I adjusted to going back to work, especially during the month when I was essentially full-time.

To be honest, it was a little scary how easily I went back to the old routine of getting up when the alarm rang and racing around the house to get out by a certain time. I’d had over a year of leisurely mornings waking up when I felt like it, (or really, when Jeffrey decided it was time to wake up and he’d shake the bed with his scratching. ) In retirement I tend to ease into my mornings, staying on the couch until 9 or 10, laptop on my lap and the dogs snoozing by my side.

Heavenly!

Now, suddenly I was pitchforked into day after day of early starts, one after the other. I honestly thought it would take longer to adjust back to the old routine than it did. It took the middle of the first “full-time” week and I was back in the swing of it.

Clothes organised, lunch organised, water bottle filled and my bag packed with everything I’d need for the day ahead. No lollygagging around on the internet, oh no! Pour a coffee, solve the Wordle, post a couple of Dad jokes on Facebook, check my timetable to see what the day will hold and then it’s off the couch and into the shower. Keep moving! Time is ticking!

In the car, podcast on. Driving on the freeway, having a goal in mind of being at the last main intersection before school at 8:20. Winning if I shave a minute or two off that time. Walk into school, grab a laptop and keys, up to the staffroom to see what’s in store for me today. A couple of minutes before the bell, start walking to the first classroom to let the kids in and be ready to call the roll at 8:50 when the bell goes.

It’s honestly like riding a bike.

The ease of slipping back into that old rushed routine was, as I said, a little scary. I’d absolutely adored my 2021 year of being absolutely free and it was astonishing how quickly it was overtaken by the requirements of the work routine. Even the little woofs quickly worked out which day was going to be a “Mum’s home” day or not. During 2021, every time I left the house they’d freak out and wait for me all day, if necessary. Since I started work, Ryan27 says that it took a week before they went back to their old routine of sleeping through the day and only starting to wait for me at the front window at about 4PM.

We’re all conditioned by The Man!

It’s not just the blissful retirement morning routine that was affected. After a calming 2021 free of the tyranny of having to fit things in on the weekends, I was suddenly doing the ironing on a Sunday afternoon, making sure I did the bread baking (for lunches) on the weekends, and generally cramming all of the activities that I used to spread luxuriously through the working week all into two days.

I realised that I was starting to think, “I don’t have TIME for this!” whenever something went even the slightest bit wrong. Apparently, I used to say that a lot before my retirement. Time suddenly switched from being my beloved friend to my enemy.

Once I’m at work, my days are a strange mix of watching time drag and being really entertained. There’s no denying that I talk to a hell of a lot more people when I’m at school. The kids are always funny and up for a bit of banter, while my free times are spent chatting to work colleagues and having a laugh.

The social side of going back to work is lovely. Don’t get me wrong; I adore my hermit life at home, but I’m also enjoying being with the people at work.

The downside of being with people is that I’m mixing with around 900 of the hormonally challenged. Yes, I’m talking about teenagers.

Now, teenagers are sometimes hilarious, sometimes deep and sometimes thoughtful. The kids at our school are, for the vast majority of the time, polite, considerate and lovely. However…

… occasionally you’ll strike a kid having a bad day. They don’t WANT to be told to do their work, they don’t WANT to be quiet and not disrupt the class and they’ll be DAMNED if they’ll listen to a ‘sub’.

Ugh.

As I’m in the middle of doing the dance that is maintaining control of the class without pushing this sort of kid into open rebellion, I’m thinking, “What the hell am I doing here? I don’t need this shit. I could be doing anything else right now…”

Or you’ll have a class at the end of the day or week who are just over it. Their regular teacher has left screamingly dull work for them to do and all they want to do is get through the next 48 minutes so they can go home. Low-level talking gradually rises in volume as more and more kids switch off and start talking to their friends. It seems like every 3 minutes I’m saying, “Ok year 8! Too loud!”

And I’m thinking, “I know. I’m bored. I feel it too. Only 15 minutes till the bell goes and we’re free! Oh no. I’m clock watching again.”

Man! Clock watching is definitely a THING. When you’re a regular teacher you have to be conscious of the time. Every lesson has an arc and you have to know where you are within that 48 minutes to drive the lesson to a successful conclusion. So clock-watching is a necessary part.

CRT is a different beast. I enter the room, call the roll and introduce the lesson. Then, unless kids have specific questions that I can help them with – which is never when I’m taking a Maths class- the rest of the time I’m pretty much making sure that the kids stay on task and aren’t misbehaving. I find that I’m watching the clock a lot. Not in a productive “lesson arc” way but more of an “oof, there’s still half an hour to go… I could be doing anything with my time… hmmmm, if I was home right now, what would I be doing?”

I REALLY don’t want to get covid and, as we all know, working in schools is a high-risk thing to do. I’m one of the few teachers to mask up. I wear a KN95 mask from the moment I get out of the car in the morning to when I get back into it at the end of the day and this, coupled with being triple vaxxed and vaxxed for the flu, has so far kept me covid safe.

(Touch wood, as my grandmother would say.)

But then, every fortnight I get paid. I like getting paid.

In this post I designed a chart to track where my earnings were going. So much more motivating than just plodding into work every day! I’ve modified it slightly since then, but I’ve basically worked my way down the chart “paying off” every item in turn.

Of course, the money I earn usually goes to my credit card, which I always keep in the black, to pay for our day-to-day expenses. But this protects my savings, which is incredibly important. Six months into a market downturn, I haven’t had to sell any shares or touch any savings or emergency fund money due to the combo of earnings and dividends. I’ve even been able to top up my savings.

This makes me feel very good.

Later on today, I have an appointment with a travel agent to find out about airfares etc to Easter Island and Ushuaia for my Antarctica trip in December. I know I should probably bring a defibrillator with me to start my heart after I hear the prices. I’ve already earned 2K towards airfares, but now that I’m definitely going to Easter Island, I’ll be adding an extra line to that chart for lots more funds needed.

Tom30 is looking to buy a place of his own and is living here to turbocharger his deposit savings. I’ve offered to give him 5K in lieu of wedding costs and lend him a further 10K if he needs it. I’m chipping away at that 5K on the chart – just under 3K to go!

I won’t deny – knowing that giving up some of my days to be able to provide extras for myself and my family without tapping shares during a bear market feels like a good trade-off long term. Knowing that I’ve actioned the flexibility in my FI plan is satisfying.

Would I have gone back to work if we were still in a bull market?

That’s an interesting question.

The catalyst for me starting CRT work was that I heard that the school was desperate for CRTs because so many staff were getting sick. I owe the school BIG TIME for the financial security I was able to build for my boys when they were kids. Part of why I went back was that I was giving back to the place that had saved our financial bacon, back in the day.

I think that I still would have gone back, but I would probably have worked fewer days. Still, I can’t deny that it was interesting to see that I still had it in me!

After working off and on for 3 months after experiencing nearly 18 months of retirement, I have to say that it’s been ok. In fact, it’s been better than I expected. To be fair, I have a huge amount of flexibility. I can say “no” to work whenever I want, and if the school doesn’t offer me enough work I can always work elsewhere as well. There are many, many secondary schools in Melbourne!

The feelings of regret over my loss of freedom in the days when I’m in the classroom are definitely offset by the security offered by an extra income stream during a market downturn. I absolutely know that I did the right thing when I decided to pivot. I’ve had too many years of being terrified by my financial situation to want to risk having sleepless nights again! A few days back in the classroom in the early days of my retirement is a very small price to pay for the huge benefit of feeling like I’m doing the right thing for Future Frogdancer’s financial security in her golden years.

The intangible positives of returning to work are a nice bonus. I enjoy 98% of my interactions with the kids and I work with truly lovely people. I’ve met some other CRTs who are great, but I was always too busy to sit down and get to know them when I was a ‘real’ teacher. I also like the pattern of the days as a CRT – you are given every single period on AND a yard duty, but at the end of the day you can walk out right on the bell, instead of having to attend meetings etc. I’m getting home at a reasonable time nowadays – with no marking!

My mindset about this shifted when it occurred to me that my 3 year stash of living expenses that I’ve put away in case of a market downturn could be stretched indefinitely if I earned just half of my yearly expenses doing CRT.

How many days a week would that be over the first 3 terms of the school year? (Term 4 is pretty much a write-off for CRTs. Once the year 12s start having their exams, the year 12 teachers start taking all the spare classes.)

Two days a week. That’s all it would take.

Hmmm. Interesting…

… Or I could get sick of it and decide to simply stop doing it. Financial Independence is a wonderful thing.

This thought occurred to me when I was sitting in a year 8 classroom earlier today, watching as they were silently reading at the beginning of the class. Normally, I’d be reading right alongside them, but I’d intelligently left my book in the car and so I was waiting for the 10 minutes to be over.

As I drew my gaze back from the window with the beautiful sunny day outside, I saw that a couple of kids were looking at the same view. Two boys were yawning, so clearly they’d picked dud books and were bored. But the rest of the class were buried deep in their books.

As I looked at the bent heads, I started to wonder where they all were.

Some of them were reading from the class novel, ‘The Outsiders‘ by S E Hinton, preparing for the work that they were going to have to do in the rest of the class. I knew they were in 1960’s Chicago. But looking around at the others, they could have been anywhere.

Far into the future, perhaps? Way back in the past? Maybe they were experiencing life from the point of view of a different gender or nationality. All of us were physically together, but within their minds they were anywhere but here.

Once their 10 minutes of wide reading time was finished, I wrote the saying I began this post with up on the board and we had a quick chat about it.

The thing is – this saying doesn’t just relate to novels. It also relates to any kind of reading, but of course, seeing as this is a FI/RE blog, I was thinking about financial independence blogs and books.

I think it’s a real shame that the Australian government has chosen to throw the baby out with the bathwater when it came to the new rules they’ve put in place about fin-fluencers. Strong Money Australia and Late Starter Fire are two bloggers who have written about this, and they’ve both done a good job. I don’t need to repeat what they say.

It saddens me, though, that these new ‘guidelines’ about what we can and cannot say are going to take valuable stories about life experiences away from those people who can learn from them. When most people realise they need to get their sh*t together when it comes to money, they are scared and worried.

I think, like most people in this space, I started to learn about investing, the stock market, financial independence etc from American bloggers and Australian books. American content is all very well for gaining an understanding of the basics, but when it comes to knowledge that’s applicable to Australia, there’s no substitute for Australians sharing their knowledge and experience.

When I first started blogging on my personal blog back in 2008, I was part of the crafting/gardening niche and it was wonderful. So many people sharing their knowledge and inspiration online, helping each other and creating a really supportive community. It was wonderful – and still is.

I was so happy to find a similar space for the people interested in gaining financial independence. Clearly, our life stories are all very different, but that didn’t stop me gleaning what I could use in my own situation, while enjoying watching people’s stories unfold.

Over the years I, a single mother of 4 boys on the shady side of 50, have learned so much from the blogs of Australians who lead lives vastly different to mine. Let’s face it – not many people have travelled the same pathway to financial independence than I have! If I was holding out for information from someone who began their journey with 4 boys under 5, $60 cash, and was driving an ancient Tarago whose sunroof leaked when it rained, I’d still be sitting around, 8 years later, terrified about how I was going to prepare for the future.

Instead, I’ve learned from single people in their 20’s and 30’s, coupled up people without kids, and coupled up people WITH young kids/teenagers/grown families. Some of these couples are married, some are not. Some are straight, some gay and some don’t disclose. A few are older than I am, and I learned a lot about what retirement life is like and what to prepare myself for.

Some write under a nom de plume, others (like me – obviously) write under their own names. Some have degrees, while others have barely finished secondary school. Most seem to live in cities on the east coast, but there are also people living in regional towns or in the bush.

We’re all very different but we all have one thing in common – we want to learn about how to handle our finances responsibly and we want to help others by sharing what we’ve learned.

The huge variety is a strength. We all come to this problem of how to gain financial independence with different ways of thinking, because we’ve all led very different lives. This means that someone who has come at this whole “FI/RE” thing from a totally different angle to you can offer valuable insights into angles that may never have occurred to you.

Sure, it may be a little confusing at first, but it doesn’t take long to sort the wheat from the chaff. I know that the more I read – and listened – the more familiar the concepts became and I was gradually able to move forward with a growing confidence that i wasn’t going to muck things up.

One of the most interesting things about hanging around in the space over a few years is to read when people have decided to pivot in their financial independence strategies and they give their reasoning. One of the most fundamental tenets of the FI/RE movement is the importance of flexibility and being able to change what you’re doing if the situation demands it – or if you discover better information.

My fear is that now that the rules have changed, people will be too scared to share valuable insights and information that could add value to the whole space. People coming up, like my sons, won’t have the same freedom to information willingly and freely shared, that I was lucky enough to benefit from.

I’m not sure where we go from here. Some people are massively editing their blogs and removing specific bits and pieces that are suddenly forbidden for public consumption. Podcasts are suddenly in hiatus (or stopped altogether) while the podcasters work out where they now stand.

Fortunately, due to me being scared of numbers and also – as a single woman – being very conscious that there are a lot of crazies out there, I was never granular about the topics I talked about, so I think this tiny blog should be ok.

I’d like to thank all of those creators who enabled me to live many lives as I was navigating my way around this financial independence thing. Your work has been so very huge in enabling me to gain my freedom and to provide a secure base for my sons.

I first learned the value of having what I then called a ‘Buffer Zone’ back in the days when I was newly separated, with 4 small boys under 6. When we split, we had a mortgage, 2 old cars and $120 in the bank. I withdrew the money and gave him half, so we each had $60. I took the people mover and he took the van he needed for work. We agreed that the boys and I would live in the house and in lieu of child support, he’d pay the mortgage.

(Anyone who’s ever been in this situation, or knows people who have, knows what’s coming next. It’s the classic move of the non-custodial who wants to punish their ex.)

Establishing a new life with $60 and 4 kids isn’t as much fun as you might think. We were able to get the Sole Parent’s Pension, as it was called then, so basic bills were covered. But I had a huge urge to get some security for us and so I decided to scrape together one thousand dollars as a ‘Buffer Zone’ for us.

It took 4 or 5 months but I did it. I scrimped and scraped, I barely ate any meat during this period – though I remember cutting off the end of a sausage that the boys were having as part of their spaghetti and ‘meatballs’ meal and devouring it. Any way that I could save money, or at the very least wring every cent’s worth of value from each dollar, I did.

And yes – one day I checked the bank account and there was $1,000 sitting there.

I breathed a sigh of relief. We had our Buffer Zone. Job done!

But something was niggling me. A few days later, I decided to call the bank and check on the balance of our mortgage.

I felt like someone had pulled the rug out from under me. The person on the other end of the line told me that the mortgage hadn’t been paid for a couple of months and that the account was $963 in arrears.

“After another month, we would’ve called to discuss it.” But of course, I wouldn’t have been the one they would’ve called. This was 25 years ago – the male name on the mortgage would’ve received the call. I was lucky that I decided to check.

But of course, I didn’t feel lucky at the time. As I threw the younger kids into the massive double stroller I had and began to walk up the street towards the bank with the older two boys skipping along beside me, I was furious. Actually, I felt incandescent with rage.

But I also felt thankful that I had the money behind me to fix it. A simple transfer from my Buffer Zone account to the mortgage and the situation was safe.

And that’s what a Buffer Zone/Emergency Account is for.

To save your bacon in the event of an unexpected expense.

Scout’s a big fam of the Emergency Fund – with good reason.

Naturally, I immediately began work on building that Buffer Zone back up. It was even harder this time because I was now paying the mortgage on top of everything else. But like everything else on this FI/RE trip, if you keep at it step by step, you eventually get there.

Would I ever be without an Emergency Fund again? Hell, no! That thing not only kept a roof over our heads when we were at our most vulnerable, but every now and then over the years it’s smoothed the ride when surprising things happened.

What about the day I loaded the boys into the Tarago and swung the roller door closed, only to have it keep on going and the bottom half swung off the car? Ok, I admit that it was stressful trying to secure the door well enough so we could drive home safely, but the next day, thanks to the emergency fund, I was able to get it fixed.

(When it happened, the boys stared at me in shock as the door was swinging wildly from one hinge. I remember thinking, “I can either laugh or cry.” With those little boys looking at me, all I could do was start laughing. The situation was so awful as to be hilarious. )

The time that Scout swallowed a seed pod and almost died was another one. Her surgery cost $3,200. I was telling that to a friend at work and she gasped and said, “I’d never be able to afford that. The vet and I would have been having a very different discussion.” Fortunately, I have a separate emergency fund for the dogs, so money wasn’t an issue. Three years later, we still have our little girl who makes us laugh every single day.

A couple of years ago I leapt blithely into my morning shower – only to leap straight back out, screaming. The hot water system had died. Three days later we had a continuous gas hot water system installed – luxury! I tell you – I loved my emergency fund when I took my first hot shower.

These are just a smattering of the times that problems that can be fixed with money were taken care of with minimal stress and no debt.

New fridge.

Over time, as I became more financially secure and started work again, the size of my emergency fund grew. It started out at $1,000, then grew to $5,000 and then up to $15,000, before settling down at my current level of $10,000.

My gauge of how much cash for an emergency I need to have behind me is pretty much the ‘can I sleep at night?’ test. With 10K, I feel that it pretty much covers most things that could go wrong with my house and car. As I mentioned before, I have a separate account for the dogs that I set up when I got Scout and then found out about the 25% risk dachshunds have of getting IVDD. I’m devoutly hoping I never have to touch that money but it’s there if she needs it.

The Emergency Fund is a funny beast. In my experience, I can go for YEARS without tapping into it, to the point where it almost feels like a waste having all that money just sitting there earning next to no interest.

Then WHAM! Something happens. Or two things happen. They seem to come in waves.

Consider the last 2 weeks. My fridge dies. After weighing the options, I decide to buy a new one. $1,900 later, the shiny new fridge is installed in my kitchen. No credit card debt, no drama. Excellent!

A week later we experience the first cold snap of the year, so we try to switch on our gas ducted heating. Nothing. Turns out that it was a 20-year-old model that has valiantly served its time but was now up for renewal. No problem. $3,000 later, a new model was installed on the same day.

Annoying? Yes. But stressful? No.

In the space of 2 weeks, I had 5K of unexpected expenses. I don’t know about you, but for me, that’s a little more than simple walking around money. Over the next little while, I’ll steadily pump money back into the emergency fund until it’s at the ‘can I sleep at night?’ level again – ready for next time.

Because we know that there’ll always be a next time.

The brilliant thing is that there are no set rules.

YOU decide how much money you want to have in there – the ‘can I sleep at night?’ rule is totally individual. Some people, particularly those with insecure or erratic jobs, like to keep 3 – 6 months of expenses in there. Some like to have a year. Personally, because the job I had was incredibly secure, I was happy with the 10K – 15K level.

YOU decide where to leave it – my personal choice is to put it in an online bank account away from my everyday bank, so it’s not always in my face. The Emergency Fund is intended to lurk in the background like a benevolent stalker until it’s needed, not to be a constant temptation to spend the money on fun stuff.

The only requirement is self-discipline. First to build up the thing in the first place; then to not tap into it unless it’s a genuine surprise expense that’s popped up. But as we all know, fiscal discipline and delayed gratification make you stronger.

The Emergency Fund is like having a friend who is always ready to have your back. And who doesn’t like that feeling?

So far this fortnight, I’ve worked 7 days. It’s been an incredibly busy time for the school, what with a huge year 7 camp, (taking nearly 500 kids away requires a lot of teachers as well), covid absences and a nasty throat bug doing the rounds.

I’m spending the whole day wearing a mask. In fact, probably the most dangerous part of the day is when I eat my lunch. For the rest of the time I keep my mask firmly attached to my face. With the mask, me being triple vaxxed and the students being double-vaxxed, I figure I’m as safe as I’m likely to be.

I’m booked to work a day next week and after that, who knows? That’s the joy and terror of doing casual work. When I was picking up my chromebook and keys from the Daily Organiser, she said that I’d put up my hand to come back at just the right time, because the last two weeks have been awful for staff absences.

She warned me that things will probably calm down and there won’t be as much work on offer, but I said, “That’s fine. I figure I’ll make hay while the sun shines. I’m using this work to help pay for Jordan’s wedding, so any work you can give me is great.”

Yes! Remember that chart I drew up about things I can ‘pay’ for with my CRT earnings? Going on those VERY loose figures, by the end of today… or maybe by the end of the day’s teaching next week, I’ll have “paid for” the first few items on the list and I’ll be up to the first big amount – the wedding.

This sort of stuff is very motivating, at least for me. I won’t lie – this morning when the alarm went off in the wee hours for the fourth straight day, it wasn’t a joyous moment. A couple of possums had galloped over the tin roof at about 2 AM and Scout vehemently objected. It took us both ages to go back to sleep. Dachshunds grumble a lot when they’re unhappy.

But when I thought about being able to cross off the boring stuff on the list and then be able to get started on the wedding, I had a spring in my step that definitely wasn’t there before.

A thing I’ve noticed that I didn’t expect at all was that in the 7 days I’ve been back at work, I’ve been bored far more than during the whole 15 months I was at home, living the retired life.

I think it’s because when you have total freedom over how you spend your time, the instant you even get a slight inkling that you might be getting bored, you can immediately drop whatever it was you were doing and move onto something else. It happens so quickly that, most of the time, the niggling feeling of boredom never gets a chance to eventuate.

Here? A successful day for a CRT means that there are long tracts of nothing much happening. You’ve brought each class in, settled them, set up the lesson and then let them go on their way. Sometimes you’re actually teaching, but more often than not you’re walking around the room making sure they’re staying on track and not watching the basketball or playing games on their chromebooks.

Given this, there have been long minutes of looking out the windows, watching the clock and generally counting down the minutes before the bell. Once every couple of days or so, I might have a therapeutic bellow at a naughty kid, but honestly, even the naughty kids at this school aren’t awful. They respond really well to discipline given with humour, so there’s rarely a need for a raised voice.

Now, it’s not as if I’m bored all the time. Of course I’m not. (I wouldn’t turn up to do CRT again if I was!) The kids are funny and I’m introducing a variety of different lessons that sometimes makes me quietly do some research into something-or-other that sounds interesting that I’d never think to learn about by myself. I just had a lovely chat with a year 10 Lit class about ‘Pygmalion’ vs ‘My Fair Lady’, which I thoroughly enjoyed.

(Pygmalion is the play that the Audrey Hepburn/Rex Harrison movie ‘My Fair Lady’ was based on. It’s fabulous – though when I read it, years after having seen the movie, I was shocked by the ending. Now that I’m older, I think that George Bernard Shaw’s original ending to the story is far better.)

Even though I’m having fun in classes like this, the contrast between my work days and my retirement days is pretty noticeable. Usually, at home I’m surprised by how quickly the day has sped by. At work, I know to the instant when that last bell rings at 3:10 and I can walk outside to my car and start living my ‘real’ life.

To be fair, I was talking just a few minutes ago to a friend who’s also come back to do some CRT. She’s the opposite – she was getting bored at home and she loves the CRT life. It’s her new hobby. We had a laugh about how different we are.

So far, I’m really enjoying being back at school and seeing the kids and staff. I’ve only been doing it for a couple of weeks so I’m definitely in the honeymoon phase. I’m still in the stage of kids getting excited when they see me and being pleased when I turn up to teach their class.

Sadly, this will fade. Soon I’ll be just another ‘sub’ who is part of the furniture. Hopefully, I’ll get enough work to take care of the wedding and beyond that, who knows? I wrote a post a few years ago about the importance of protecting your savings, so maybe I’ll continue to do a day or two a week, paying for outgoings as I go and keeping my savings for the Big Fun expenses, like travel.

(Actually, before I posted that link, I re-read the post. It’s got some pretty good points in it, if I do say so myself.)

I’ve always felt very lucky that I fell into a career that I was good at and I genuinely enjoy. It seems that CRT has most of the good stuff and very little of the bad stuff. I’m interested to see how this all pans out.

Retirement Reading Quest – Reading my way to ‘free’ council rates.

I’m on a quest to borrow and read enough books to, in effect, cancel out the cost of my council rates per year.

It’s outlined in this post.

Years 8,9 and 10: 2016/17/18 – $5,400

I may as well continue back-tracking. I moved here in 2016, so I’ll chip away at all the rates I paid up till then. I’ll need $5,400.

Running Total – $2,125.

Year 7: I’m already a year ahead on my rates, so I’m taking a reader’s suggestion and I’m going to go back and start covering the rates from the year before I started. I may as well.

Year 7: Total needed: 2019/2020…$1,800

Finished! 12/12/2025

Year 6 (2025/2026) $2,590 AREADY COVERED!!!!!!

10/08/2015 – I won’t have another rates notice until August 2026, so I have time to kill. Let’s knock over a previous year’s rates, just for fun.

Year 5 (2024/2025) $2,339 and dog rego ($63) = $2,435.

Finished it before I even had the new rates notice ready.

Year 4 (2023/2024) $2,413.

Success! Not sure exactly when I passed the total, because I was waiting on the dog registrations to come through. But yes – I blitzed it.

Year 3: (2022/2023) $2,350

12/01/2023 FINISHED! Not working gives me heaps more reading time – I recommend it!