I’ve had an emergency fund for the last 2 decades. When I left my husband 22 years ago with $60 cash in my hand and with 4 boys under 5 to support, the first thing I set myself to achieving was building a $1,000 ‘buffer zone’ (as I called it then) to provide some security for the boys and me. I’ve written about how an emergency fund is a very good thing to have but is this still the case?

It’s been interesting to see how having that stash of cash has made life so much easier in this pandemic.

When, in December 2019 and January 2020, news started coming out from China, then Italy about this weirdo new virus, my spidey senses started tingling. I’m a bit of a germophobe at the best of times, so the thought of having to deal with a possible pandemic wasn’t a great feeling. Add to that my job as a teacher, being surrounded by germ-ridden teenagers all generously sharing their viruses with everyone around them – it meant that I was paying attention to what was going on.

Over January and February, I didn’t use my Emergency Fund at all. I quietly topped up on staples and non-perishables as part of my normal shops. By the beginning of March I was looking to be in good shape. I took a little holiday and enjoyed myself. Then, a week or so later was when the proverbial hit the fan. You remember – when people started panic buying toilet paper, flour and tissues.

The middle of March was the first time I deployed my Emergency Fund. The last time I tapped it was the beginning of 2019 when Tom28 needed a loan to repair his car. He paid it back within 2 months and then the emergency fund just sat there, biding its time.

Remember when I wrote about going to Costco the day after our state Premier announced a state of emergency? As David26 and I rounded the corner after parking our car and saw the 1,000+ people ahead of us in the queue, I decided that if we were going to brave this, we were going to make it worth while.

In the back of my head were all my fears about the ‘just in time’ policy that our supermarkets have. For years I’ve been telling the boys that you don’t want to be out panic-buying supplies when everyone else is fighting for them too. Far safer to be at home while everyone else is wild-eyed and desperate. That trip to Costco was illuminating. Turns out I was correct.

We were only there in the first place because David25 wanted to bring some supplies to his girlfriend’s family. Ok, fair enough, but I was damned if I was going to race around behind one of those huge Costco trolleys, dodging hundreds of last-minute panic buyers just to buy things for other people! If I was going to be doing this crazy thing, I was going to top up our own supplies as well.

So we bought bulk bags of plain flour, bulk dry pasta, another big bag of grain-free dog food, oil, eggs, coffee, cleaning supplies… between what we bought for Izzy’s family and ours we loaded up the trolley.

On the way home we passed Dan Murphy’s. Seeing as we were already stocking up and it was definitely a ‘Spend Day,’ (more on that later), we turned in. There were only about 6 other people in the whole place. We were definitely ahead of the trend in buying alcohol! We bought heaps of wine, ( I don’t want to do without my shiraz in the evenings!) and I shouted David26 and Ryan25 some vodka, beer and spiced rum.

Earlier that day, at 8AM, I’d been to Bunnings, buying fence paint and potting mix. I’d thought ahead and realised that I’d need to occupy myself in the lockdown I was sure was going to come.

All up on that day we spent around 2K.

That’s when I deployed the Emergency Fund. I pulled 2K out from it and put it straight onto my credit card. I didn’t have to go into debt to shore up our defences – we had the cash. After all, if a pandemic isn’t classed as an emergency, I don’t know what is!!!

But then came something else…

A week after we went into iso, my oven broke down. Great timing, hey? It had come with the house, was cheap and nasty and was always something that I was going to get replaced, but I wasn’t planning on doing it any time soon.

Now this WAS an emergency. I’d just begun a sourdough starter – I needed an oven to cook in!

This was where the Emergency Fund proved its worth yet again. If I had no money set aside and had to buy something on my credit card, I know full well I would have probably bought another cheap and nasty oven – anything to get food hot and ready for dinner. I’d want to limit what I put on the card, so it would have been the cheapest I could buy. This would mean that a couple of years down the track I’d be in the exact same position that I was now – hating the oven and wanting to buy a new one.

But now? I knew that I wanted a German-built self-cleaning oven. Something sturdy and of good quality that would last for years. These ovens don’t come cheap.

I’m of the mindset that I’d rather do something right and only have to do it once, rather than trying to cheaply do things and end up having the same problem over and over. The Emergency Fund meant that I had the money there to get the job done right – first time. Sure, I was a bit annoyed at having to spend the money right now – this was a job that I would have been happy to palm off to some future time – but having the Emergency Fund meant that I could take care of it properly.

(On an aside – you should have seen the guys who came to deliver and install it a week later. They were gloved and masked – it almost looked like they were going to rob the place!!)

So the oven, plus installation, cost nearly $1,800. That’s nearly 4K to come out of that account in a couple of weeks. So how does running the Emergency Fund look like after this?

Easy.

As soon as you tap the Emergency Fund, the iron-clad rule is that you devote the next however-many-pay-packets-long to building it up again. You want to get it back to its original level as soon as you can, ready for the next unexpected event.

Sure, the timing’s been a little annoying. With that dip in the share market, I would have loved to be buying cheapish shares with my surplus money like a lot of FI/RE people have been saying that they’ve been doing, but in the Jones household financial security comes first. This means that a strong Emergency Fund is the top priority.

My next pay is on Wednesday. I have $500 to go to get my Emergency Fund back to its pre Covid-19 level. How have I done it so quickly?

Haha! My secret weapon – my ‘No Spend Days’ chart. It’s all about turning buying things and spending money from a mindless activity to an INTENTIONAL one.

I posted about how it works HERE. It’s worth reading if you think that this might be something that will help you have fun tracking your spending. It really works for me.

Basically, every day that I don’t spend anything, I get to colour in a square. if I have 3 or less days a week where I’ve spent money, I get to colour in a silver square at the end of the week.

The idea isn’t that I never spend any money at all – that’s obviously unsustainable. But what it does is to force me to consciously consider WHEN and WHAT I spend my money on. It turns spending from a constant dribble out of my wallet to a truly deliberate decision.

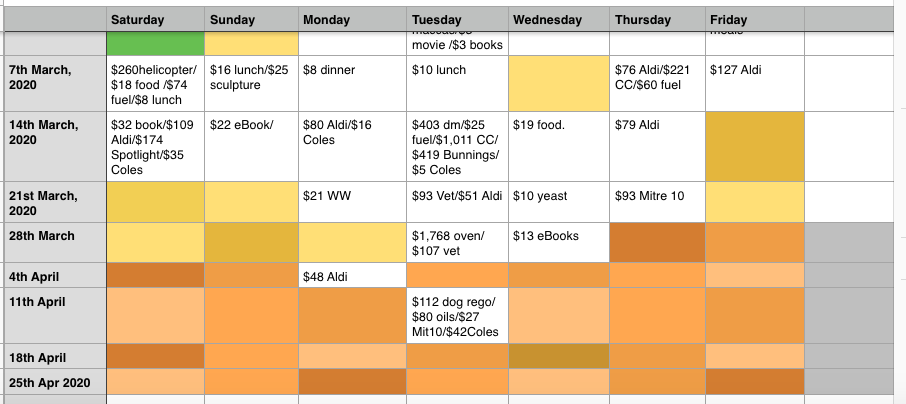

Now have a look at the screenshot I took from my chart. It’s showing March and April. April is orange – March is yellow.

From the 7th of March, I was away on my little holiday at Bowral. You can see there’s a spend of $260 on a helicopter ride – that’s not a usual item in my budget! I arrived home the following Tuesday, had a ‘no spend’ day after that where I just chilled at home… but then I swung into gear mopping up the last of the Covid-19 lockdown preparations.

On the 14th March you can see my ‘panic-buy’ at Spotlight, where I bought $174 worth of quilting supplies. A few days after that, on March 17, was the hideous Costco shop, along with the Bunnings and Dan Murphy buys. I deliberately grouped them all together, knowing that they’d be substantial. Geographically, they were close together too – saving on petrol. Why not? 🙂

The rest of March, the shopping was just for little incidentals to pick up tiny things I may have missed. An example is the $10 yeast on the 25th March.

But look at what happens once April starts:

Well ok, buying the oven on the first day of the month was annoying, as well as having to take a sick dog to the vet. But after that, the spending has plummeted. Why do I need to spend money once everything I need has been taken care of?

Some people I see on Twitter and Facebook are preening themselves on their cleverness in using online shopping to buy food and anything else they want, saying that they’re taking themselves out of the line of infection. But that doesn’t sit right with me – I think that by doing that, you’re putting other people INTO the line of infection by having to get your order to you. I know people need the work, but for me? I’d rather know that I’ve looked after ourselves and we’re not asking other people to risk their health just so we can bunker down and feel safe.

I’m lucky in that I still have a wage coming in. Most of that wage has so far been replenishing the Emergency Fund. But this is something that anyone can do whether they have a job or not – I know because I did it myself when I was absolutely broke and living on the Sole Parents Pension.

It doesn’t matter if you can afford to tip a thousand, a hundred or ten dollars a pay into building your emergency Fund back up – IF YOU KEEP ON DOING IT EVERY PAY, IT WILL GET THERE EVENTUALLY. You just have to keep the long view in mind and know that it will happen and you’ll be all the more secure for it.

As for our long streak of not spending any money, this will end tomorrow. With all of the delicious sourdough I’ve been making – (RECIPE HERE, thanks to latestarterfire’s recommendation), we’re down to our last stick of butter.

I’ll be whisking myself off to Aldi to buy butter, top up our fresh produce (though the garden has been a godsend in keeping us away from the shops – (another security measure I should maybe write about??) and to buy some chicken chips. I still have some chocolate, but nothing beats the salty crunch of potato chips/crisps when I’m watching ‘Survivor’.

In a few days my Emergency fund will be back to normal and I can relax, knowing that when – not if – the next unexpected thing hits us, the one thing we won’t have to worry about is money.

And that’s a precious thing.

Amen, sister! I also divorced 20-ish yrs ago and knowing I was the sole support for my kid was the purest motivation to get my financial self straight and build a hefty emergency fund. The peace of mind is priceless. I’ve been harping on my daughter to do the same since the day she set out after college. I guess this will be an object lesson for her and hopefully everyone else. The emergency fund is key. Along with a well stocked pantry.

I knw 2 of my kids have Emergency Funds. I’m just hoping that the penny will drop for the other 2 now that all of this has happened.

Just read that a bank took over the funds in a redraw account, which is where my funds are. So I am getting a $10,000 emergency account. Up to $5,000 at the moment.

Yikes! Seems incredible that a bank could get their hands on what is essentially extra repayments… I’d be doing the same as you.

Last October, when I finally saved enough in my Emergency Fund, I anguished over whether I was holding too much in cash – should I have invested more in the stock market? Now, I am very grateful that I have that cash available – I’ll take financial security any day!

It’s my dream too to have a self cleaning German oven – waiting for my oven to die first, haha! Those sourdough loaves look so good – baking sourdough has literally saved me during this time of stress and anxiety at work

Financial security FTW.

I think a lot of PF bloggers got too complacent during the last 10 years of the bull run and ignored the inestimable value of a healthy Emergency Fund. They’ve gone very quiet lately.

I liked the article. An emergency fund is a necessity for anyone. Even more so if there is only one income. -DP

True. Also when that one income is supporting more than one person.

Preaching to the choir! I’m so grateful for my emergency fund. This past year I’ve been maxing out investing, but did a small, regular contribution to a “reserve-sinking” fund. Now I’m thinking, while I still have a job, all extra $ goes into building that reserve fund to have at least one year’s expenses, just so I can breathe a little easier. Your experience stocking up sounds so similar to mine. I am lucky husband is able to visit a small produce stand for fresh food, it’s never crowded and safe so there is no need for big online spending/hoarding. But this is a marathon, not a sprint. Reserves are the way to go!!!! Thanks for another great post.

You’re right – it IS a marathon and not a sprint.

I was in a zoom ‘meeting’ after work Friday with some friends and we were talking about how there’s no clear end in sight as to when the coronavirus will no longer be around.

The ‘new ways’ of living might become the new normal for longer than we think.

Excellent examples of why an emergency fund is the basically the best fund. I am a big supporter of the “buy me once” movement too, financially it makes so much more sense to buy quality upfront not to mention less waste to the landfill.

I am totally waiting for a post about your helicopter flight for your fancy getaway before the Coronacation. I mean, what?!

When I saw your sourdough loaves photo I was like, when did Costco start selling that? I need to pay attention more!

Happy health and savings!

I like to try things once – hence the helicopter flight. It’s nice to now be able to look up at helicopters in the sky and actually know what it’s like to be up there.

Yesterday the police helicopter was circling the neighbourhood and instead of worrying about what might be happening somewhere nearby, I was thinking about how they’d clearly be able to see Ryan25 and I working in our front yard.

So yes – a helicopter flight is the gift that keeps on giving! 🙂

A perfect example of an emergency fund in action. You are awesome FDJ. Love the sourdough bread and the new oven. And getting to Bunnings while the Covid-19 scourge was still in its infancy was pure genius. I didn’t get my hobby and home-improvement purchases in before Covid-19 overwhelmed us, and now, save for my glorious bison, my hobbies and home-improvements are on hold. Stay strong and safe, FDJ. Peace.

And a glorious bison it is, too!

Love the idea of no spend days. I have seen the same tactic work for diets — no dessert days, no meat days, etc. We elect not to apportion our funds to emergency v. non-emergency. We do keep cash, which we look at as an opportunity chest in case something comes up we want to invest in. But we assume that there will be emergencies coming up pretty regularly (we had to replace our washer in March), and we’ll just spend less in other categories. If it’s a big expense (e.g., big maintenance needed on our apartment or one of our rentals) we do keep a low-interest home equity loan, which we then pay off quickly, if we don’t want to pull from our cash account or other investments. Yes, that only works if you’re really disciplined about not using a HELOC for discretionary spending.

Ugh. I know what you mean about emergencies popping up. In April our oven died and 2 days ago the dishwasher also carked it.

I love my Emergency Fund!